As James Carville once famously said, “It’s stupid, the economy.”

OK, that’s not exactly what he said, but he certainly could have. Maybe should have.

The economy is so unintuitive right now, it’s stupid.

In fairness, Carville’s verbatim quip was true in ‘92. Back then, people’s political choices were dictated by their views of the economy and financial well-being. Plain and simple.

Now, it’s flipped.

Political events – and the news surrounding them – determine people’s financial views today. Hope, fear, and reactionism supersede any honest assessment of economic reality.

Don’t get me wrong, macro-economics are still a crucial indicator and predictive of many other things. It’s the reason we always lead this email with our latest economic sentiment reading. It’s the reason I check our real-time numbers nearly every day. Consumer confidence affects spending, price sensitivity, credit card debt, you name it.

It’s just not the primary indicator anymore.

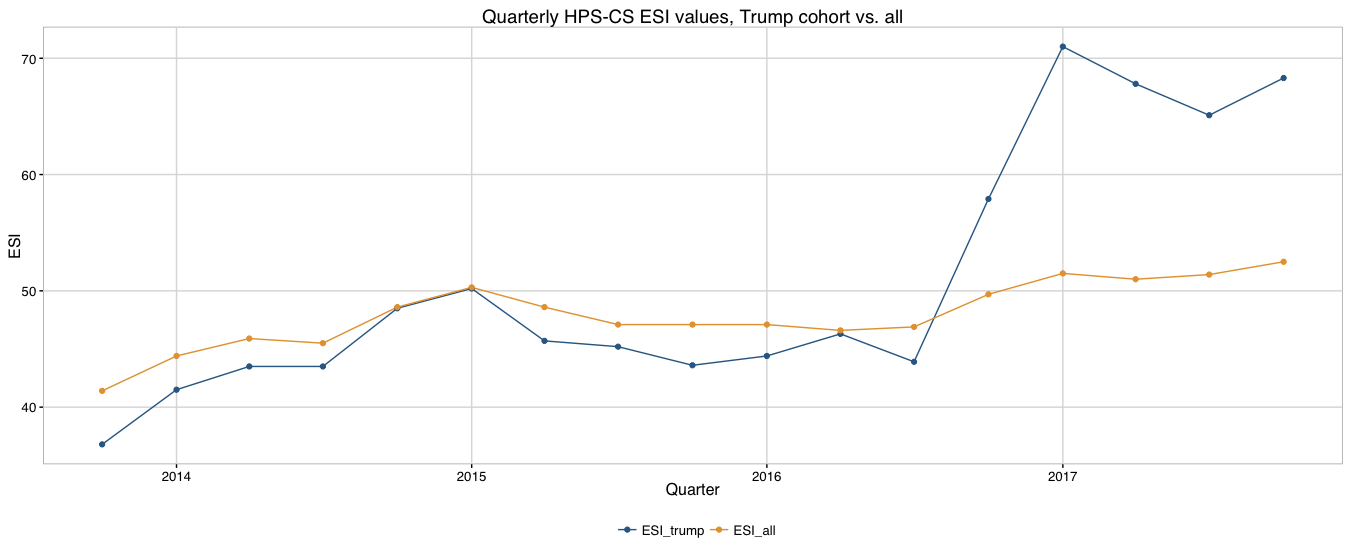

Sometime on or before November 9th, 2016 things changed. Feast your eyes on this crazy chart, showing our Economic Sentiment Index (ESI) during that period:

The blue line shows consumer confidence among people we identified as Trump voters, while the yellow one shows the full U.S. population. Both lines rose immediately after Trump won, but the blue one skyrocketed. Did those people instantly have more money in their bank account? Did they get better jobs? No. Nothing tangible changed. It was hope. That’s it.

If I showed you the same chart for Hispanic sentiment, you’d see the opposite effect. When Trump was elected, immigration policy fears took over and Hispanic consumers withdrew from the economy. Months later, companies like Target reported major declines in Hispanic spending. By summer 2017, it hit the movie industry.

From those days forward, our ESI has become a clear lagging indicator of socio-political news. It’s particularly noticeable – and depressingly predictable – when you slice the data by political tribe.

People are so glued to the news, so reactive to the latest bombshell. The COVID crisis was an exponent. Sensitivities have heightened by the day over the past two weeks.

And it will only worsen as the election approaches. Collective blood pressures will rise and fall with every public poll. Consumer confidence – and investor confidence – will rise and fall along with it. You can see it in the markets this very minute.

If anyone asks you why, just tell them.

It’s politics, stupid.

Here’s what we’re seeing:

Consumer confidence had its biggest two-week jump since we started tracking it 8 years ago. See what I mean? What kind of craziness is that? Well, truthfully, this one had some economic news behind it, namely the surprising job numbers that came out last Friday and the increased reopening of businesses. But then people said the jobs report was an accounting error. Then the Fed Chair warned of coming darkness. Then COVID cases are climbing again. The stock market jolted upward early in the week, then tanked late in the week. Please keep your arms and legs inside the ride at all times.

The restaurant industry will be the most interesting bellwether of the economic recovery. There’s a fascinating mix of news in our latest restaurant data, where we’ve seen the group of Americans comfortable eating out right now climb to 33%. It goes to 45% when we ask about outdoor seating. Still, 1 in 4 people say it will be six months or more until they feel good about eating out and that number hasn’t changed much in weeks. Incidentally, Mexican restaurants appear to have a better outlook than most. And who knows how all this will change if the latest surge in CV cases gets any worse.

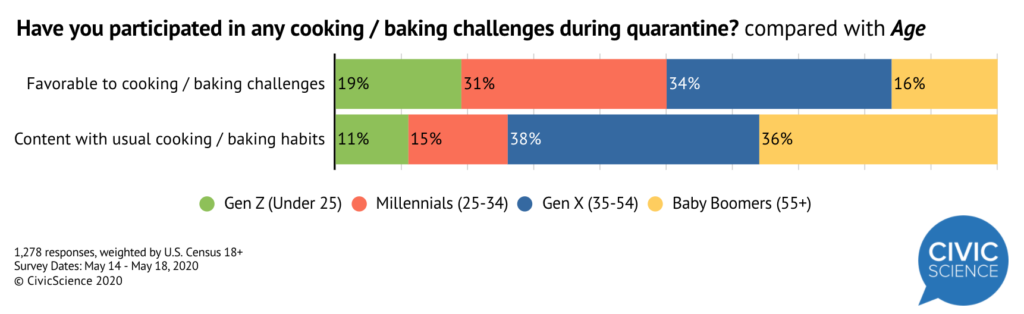

Perhaps because of their apprehension about dining out, Americans are getting way more adventurous when they eat at home. Over half of U.S. adults say they tried new foods or cuisines during quarantine. Thirty-eight percent purchased new kitchen equipment. At-home fermentation experiments have been on the rise. Sixteen percent of people have even participated in some kind of cooking/baking challenge since the COVID crisis started, even higher among Gen Xers.

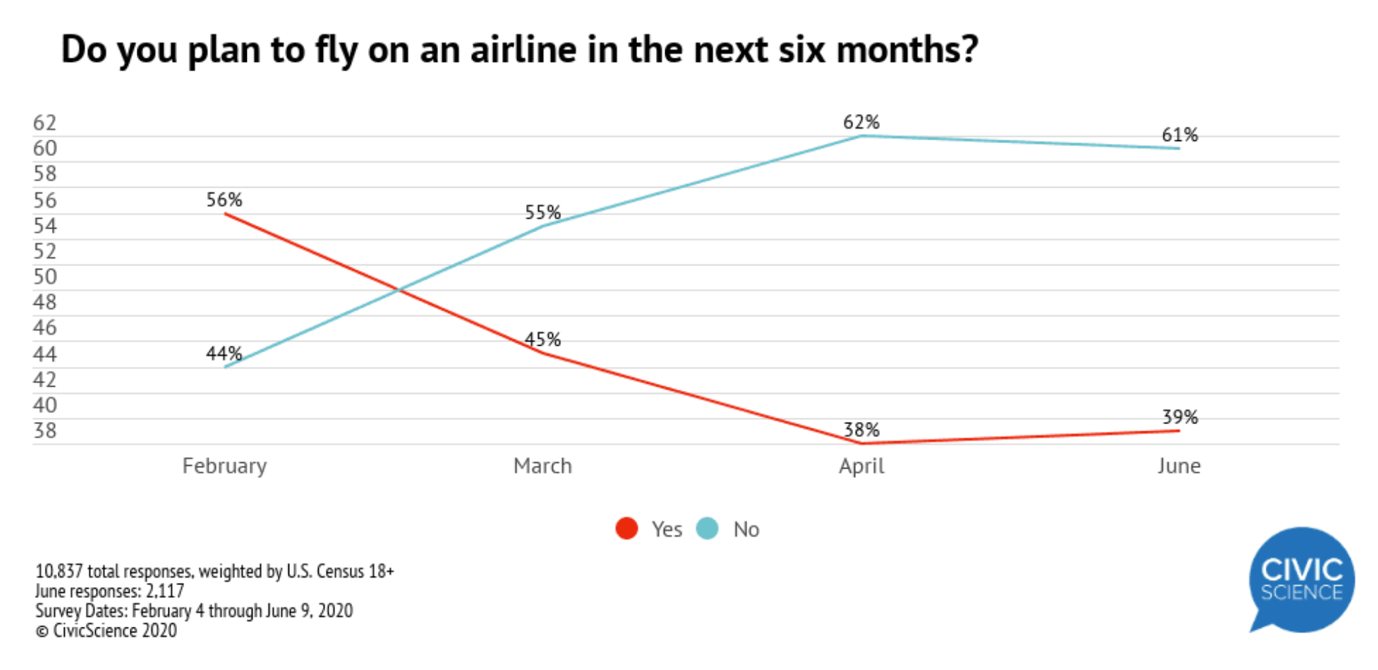

Say a prayer for the airlines. When I’m asked which industries or activities I fear for the most, I usually talk about urban commercial real estate and the performing arts first. I don’t usually bring up air travel, just because it seems so obvious. But even as we are starting to see more optimism in other categories like dining, shopping, and even vacationing, broadly speaking, willingness to get on a plane is barely improving.

Online furniture buying has seen a surge since March. When you’re stuck in your house 24/7 for three months, those old chairs and couches really start to get on your nerves. Then there’s the makeshift home office you’re trying to cobble together after constantly getting the worst working location in the house when your teenagers and wife commandeer all the prime real estate. Maybe that’s just me. But apparently not. Twenty-three percent of Americans have purchased furniture online recently, with the percentage highest among people who have been forced to work from home. Another 15% are intending to buy – which is huge, relatively speaking – and could get bigger if we don’t return to work and school by the fall.

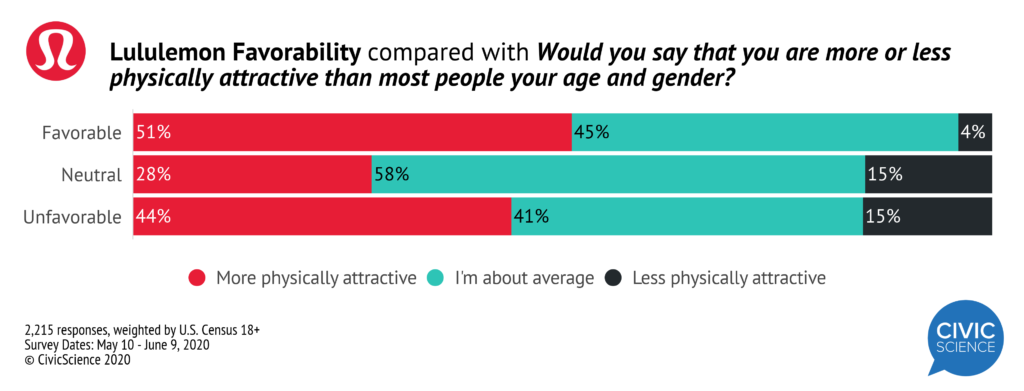

To lay around on all those new couches, people stocked up on a bunch of new sweatpants and such too. I think everyone would have guessed this one, but it was interesting to see some actual data on the subject. One in five Americans have purchased new leisurewear since the start of quarantine and 26% say they are wearing their comfy clothes more than ever. Women and Gen Z were much more likely to go full casual. In related news, brands like Lululemon also saw a boost during lockdown, especially among good-looking people. Or maybe just narcissists.

We keep churning out more great studies than I can do justice:

- Well over half of Starbucks customers are warm to the idea of the company’s new pick-up-only store concept;

- One headwind battering the airlines is the significant reticence among consumers to share personal health information in order to fly;

- We dove into the PC gaming system category, which I knew nothing about – and it’s much bigger than I realized;

- The majority of NBA fans are supportive of the league’s plan to return to competition, just not as supportive as hockey fans are of the NHL’s plan, which makes sense if you’ve followed anything I’ve said since the COVID crisis started;

- Still, nearly half of Americans say it will be 6 months or more until they will feel comfortable at a sporting event or concert. I’ll take the over.

And here are our most popular questions this week:

- What‘s better: sunbathing beside the pool, or swimming in the pool?

- Have you, personally, ever used the streaming service account of someone living outside your household without paying for it?

- How many books do you read in an average year?

- Torn jeans as a fashion statement: love it or hate it?

- Ice cubes in wine?

Hoping you’re well,

JD