I survived another Consumer Electronics Show.

I don’t know why they perennially schedule CES immediately after the holidays – in Vegas – where New Year’s resolutions come to die. Even if you’re lucky enough to avoid whatever plague makes its way around the tens of thousands of attendees, it takes at least a couple days to recover.

Still, it’s worth it. The concentration of client and prospect meetings saves me several trips I’d otherwise make to see people in person. The serendipitous encounters and networking are a bonus.

The speaker content this year was fine – if predictable and gratuitous. Let’s just say that if there were a drinking game where everyone had to take a swig each time the term “AI” was uttered, the Vegas ERs would’ve been slammed with alcohol poisoning cases.

That’s not to imply I’m an AI naysayer. The technology is nothing short of mind-blowing; its potential implications for our economy, lives, culture, and geopolitics, nearly endless. We’re exploring its applications across every nook and cranny of our business. I get it. But a lot of the companies blathering about AI at CES were simply pandering.

In what I promise will imminently be related news, Tara and I saw Maybe Happy Ending on Broadway last weekend. Taking place sometime around 2060, it’s about the adventures of two outdated ‘helper-robots’ who were retired by their human employers. It won the Tony for Best Musical last year, deservedly so. It’s quite possibly the best show I’ve ever seen.

If you think the concept is out there, I have news for you. It’s closer than you think.

In the exhibit hall at CES, I watched anthropomorphic robots wash dishes, make beds, and beat an able-bodied man at ping pong. I saw “smart” exoskeletons designed to help people with disabilities climb mountains (inspiring) and autonomous pull-carts carrying golf clubs (niche, but cool as hell).

Our world is about to change in ways we can’t imagine, likely sooner than we think.

It’s easy to focus on the potential dangers of AI, the economic bubble it will eventually cause in the short term, and the societal and geopolitical risks it poses in the long term. There are plenty of reasons to be cynical, even terrified.

But I’m trying to start off the new year on a positive and hopeful note. What I saw in Vegas this week – and the warm glow of an idyllic Broadway musical – made me excited for what the future can be.

Let me enjoy it for a week anyway.

Here’s what we’re seeing:

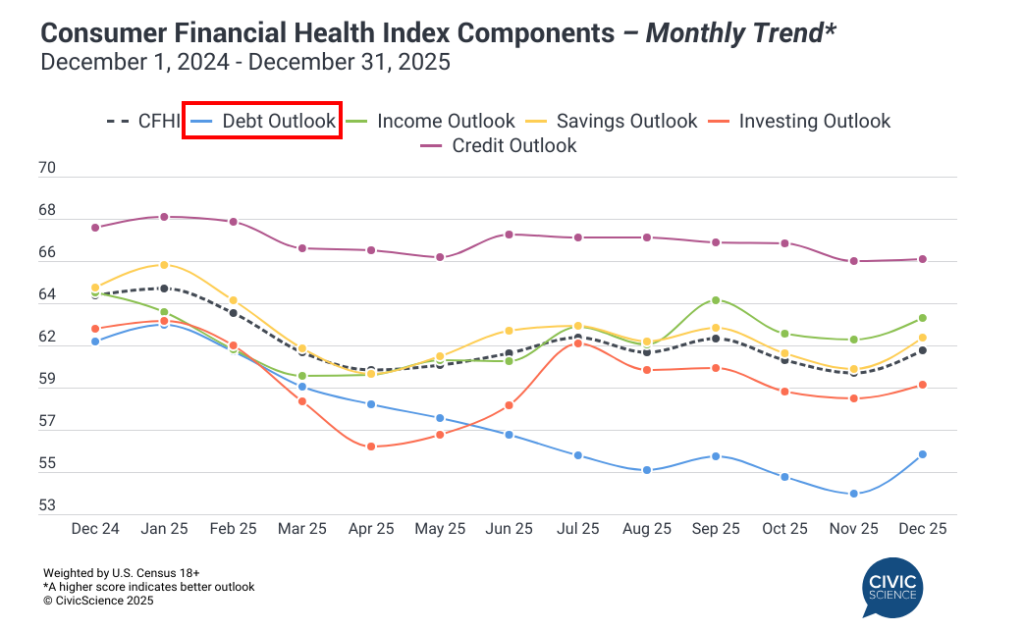

Americans’ financial outlook ended the year on a positive note, at least until their Christmas credit card bills show up. Our December Consumer Financial Health Index came out this week, showing a marked improvement over November. It was still below the levels we saw in September and way off the same period a year ago. Nonetheless, all five core metrics increased, led by consumers’ debt outlook, which moved up and to the right for the first time in over a year. Frankly, I can’t explain it, given how much people were racking up credit card and BNPL debt, but I guess time will tell.

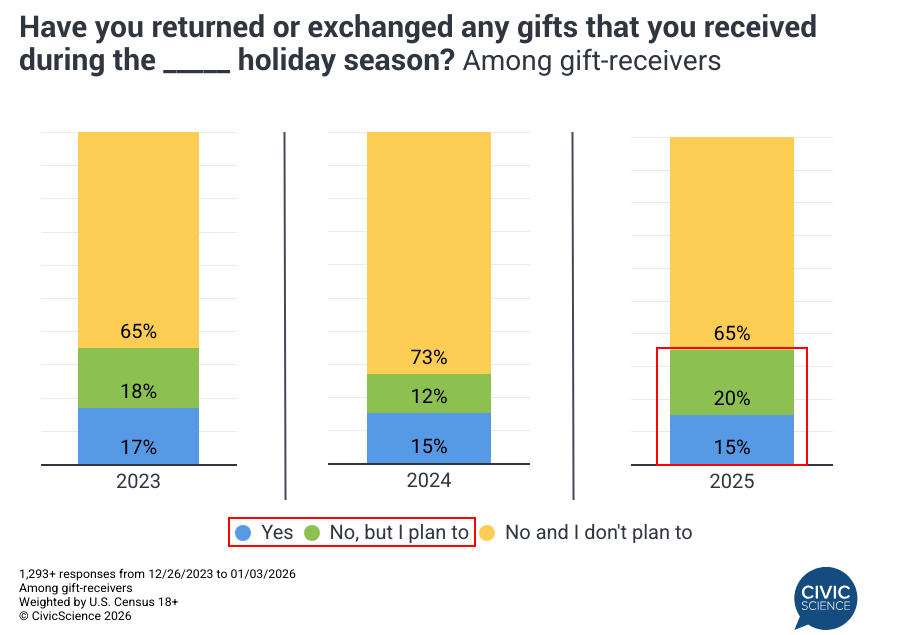

It appears a lot of people didn’t like their holiday gifts this year. Thirty-five percent of U.S. adults told us they’ve already returned one or more gifts this year (or plan to do so soon), an increase of eight percentage points over the 2024 season. Clothing and accessories lead the way, followed distantly by toys and household items. The biggest reasons respondents cited were incorrect fit/size, lack of usefulness, and duplication with something they already owned. Notably, gift-returners significantly over-index among people who are worried about repaying their holiday debt, meaning they’re also motivated to simply pocket the cash.

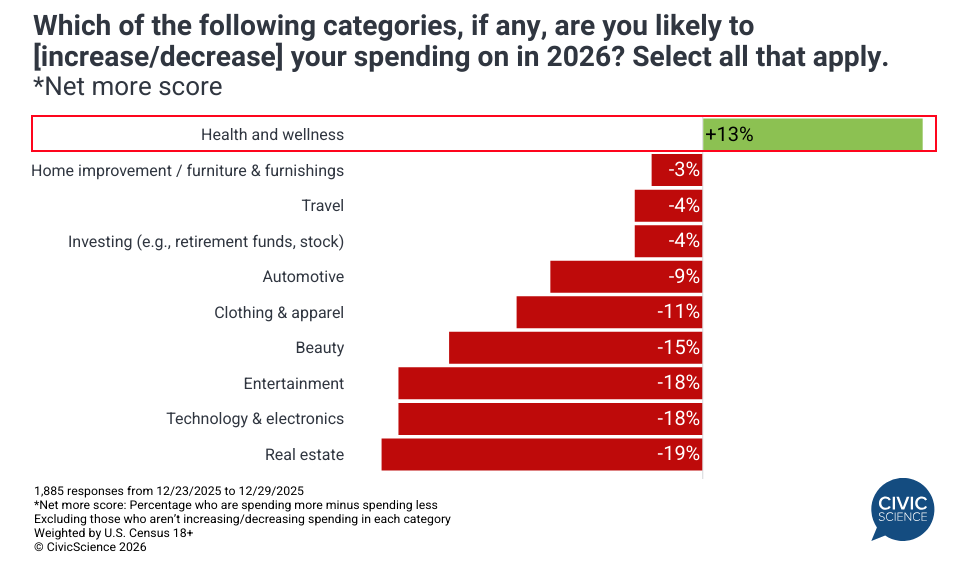

Health and wellness spending will be a high priority for consumers in 2026, well beyond their New Year’s resolutions. A trend we saw (and reported on) beginning last summer, Americans are increasingly recommitting to their physical and – very importantly – emotional well-being, manifested in where and how they spend their dollars. In fact, among many discretionary spending categories we track, it’s the only one where people anticipate a net increase in their spending this year. Also in our 3 Things to Know this week, we looked at the home improvement projects people are most likely to take on this year and shared some early numbers on voting preferences heading into the midterms.

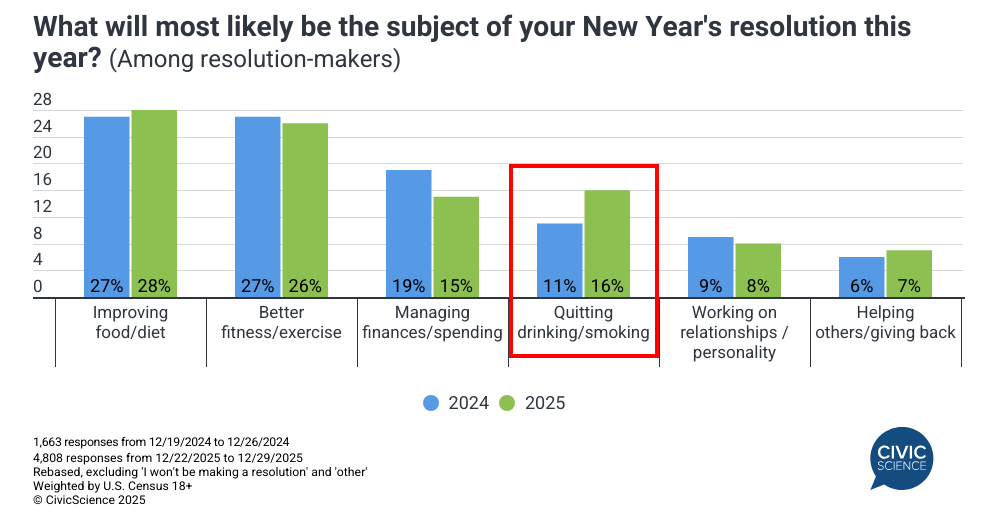

Speaking of New Year’s resolutions, cutting back on vices is the primary target this year. The percentage of U.S. adults who plan to embark on a resolution is up three percentage points over last year, led by those looking to improve their diet. Plans (or hopes) to increase exercise actually fell compared to 2025 (although I still saw plenty of strange faces in the gym this week). The biggest increase, year-over-year, was among those who plan to cut back on drinking or smoking. And, indeed, participation (or at least intent to participate) in Dry January is up yet again. The biggest decrease was among those focused on managing their spending and finances. I hope that one doesn’t come back to haunt us.

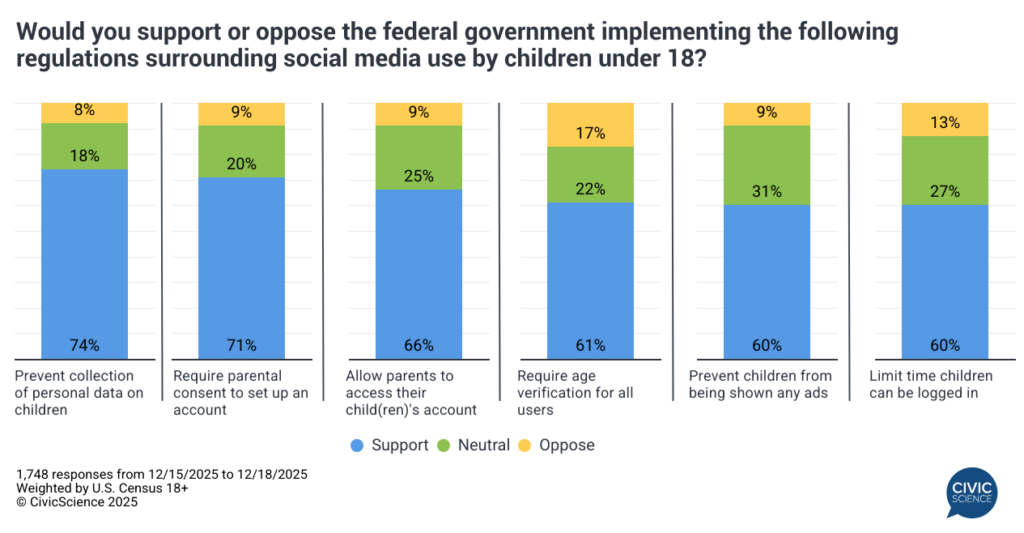

There are few things Americans agree on more than the idea of social media age restrictions. In the 3 Things to Know we published before Christmas, we looked at public support for various age-related policies designed to limit and/or protect teens and children online – and the support is overwhelming across party lines. It’s enough to make you wonder why it’s not happening, except we know exactly why it’s not happening. Anyway, we also shared data about the types of content people turn to when trying to deal with stress, as well as more insights on consumers’ spending plans going into the new year.

More awesomeness from the InsightStore™ (including a couple studies from before the holidays):

- Clothing rental services keep growing in popularity;

- Holiday meal spending was done, pre-made items were up, fewer people went out for New Year’s Eve, and a few other pre-holiday insights.

The most popular questions this week:

Would you drink a beer made from recycled water?

Do you have a favorite teacher from high school?

Are you a fan of cooking competition shows?

Do you think ‘rage bait’ marketing is generally an effective or ineffective strategy?

To what extent does flying stress you out?

Answer Key: Only if there was no other beer; Yes, Mrs. O’Halloran changed my life; Love them; Sadly, very much; At this point, I just roll with it.

Hoping you’re well.

Forwarded this email and want on the list? Subscribe here.