CivicScience engages directly with consumers, collecting over one million survey responses daily, to turn real-time insights into high-performing advertising campaigns. See how leading brands use CivicScience to drive campaign performance here.

Last month, CivicScience posed the question, “Are women okay?” The answer that emerged from our consumer-reported data was a measured “not exactly.” But while the weight of systemic stress and economic uncertainty remains heavy, the data also revealed a compelling silver lining: women aren’t taking the adversity they face sitting down; they are actively finding ways to help them feel better. As stressors like inflation and the news cycle continue to loom large, new insights reveal another way women are being proactive this year: by jumping into the investment market, turning financial intent into a form of self-advocacy.

1. One-third of women expect their finances to improve by year-end, reflecting a level of optimism that nearly reaches parity with men.

Before diving into investing, it’s important to gauge where women stand in terms of their current financial outlook. According to the latest consumer-declared data, one-third of U.S. adult women say they expect their personal financial situation to improve in the next six months, compared with 42% who anticipate it staying the same and 25% who expect it to worsen. While overall financial optimism is nearly equivalent to that of men (34%), CivicScience data show that women are managing and investing in their finances differently.

2. When it comes to current money management, 1 in 2 women say they utilize a savings account, but they’re less likely than men to use other methods, such as stocks and retirement accounts.

Women are slightly more likely than men to say they use savings accounts to manage their money (50% to 48%). However, a “utilization gap” persists in wealth-building: women are 39% less likely than men to say they invest in stocks and 22% less likely to utilize a 401(k) or other employer-sponsored retirement account.

3. Bridging the financial literacy gap is essential to overcoming the perceived barriers to investing among women.

While perceived lack of funds is a key barrier to more women beginning to invest, the data suggest it’s also a gap in financial literacy. While most women claim some level of financial literacy, they trail men in confidence. Only 27% of women describe themselves as ‘very’ financially literate, compared to 34% of men. Furthermore, women are nearly twice as likely as men to say they are ‘not at all’ financially literate (19% vs. 11%).

This literacy deficit feeds the primary deterrents keeping women on the sidelines:

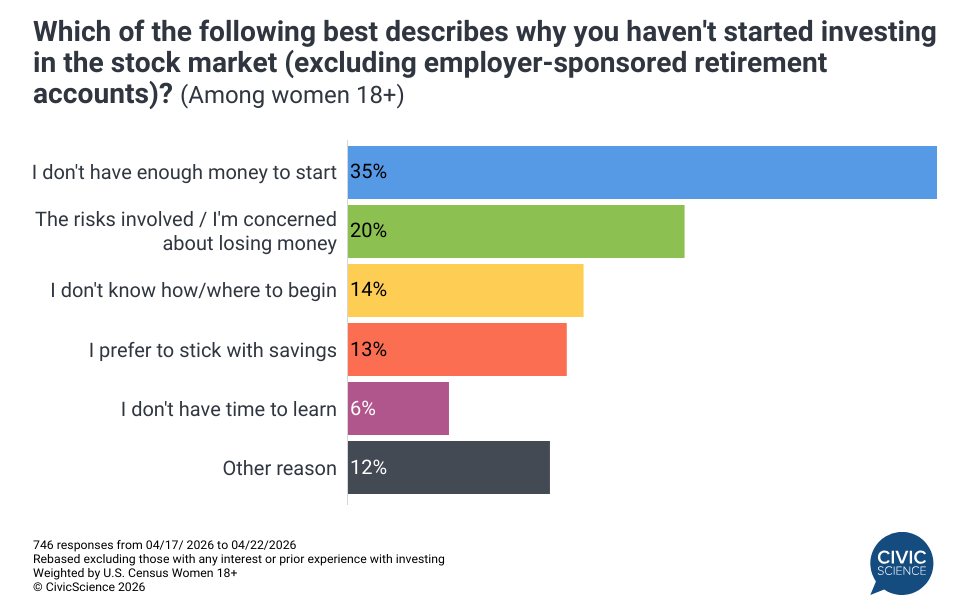

- Risk & Knowledge: Fear of loss (20%) and not knowing how to start (14%) remain major hurdles to investing.

- Cost of Entry: 35% feel they don’t have enough money to start investing.

This suggests a significant knowledge gap regarding modern investing; those less financially literate may simply be unaware of the lower-cost, lower-risk options that could support those with smaller budgets and lower risk tolerance.

4. Despite these roadblocks, close to one-quarter of American women 18+ are interested in jumping into investing in the near future.

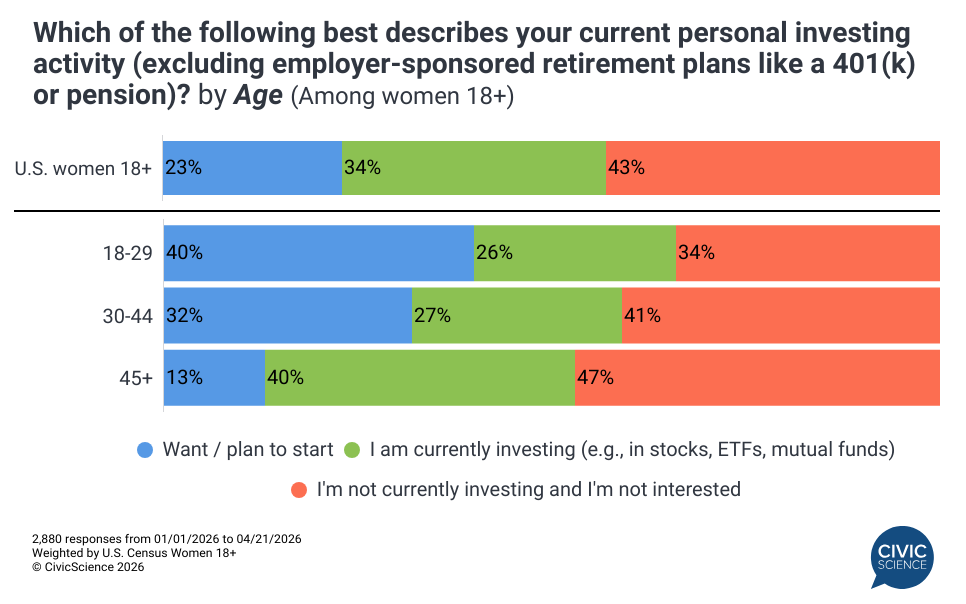

The economic climate remains turbulent, but a resilient segment of women is ready to move from the sidelines to the ticker tape. In fact, nearly one-quarter of U.S. women (18+) either have definite plans to invest within the next 6-12 months or would like to start but remain uncertain.

However, this intent is not evenly distributed across age groups. The drive to start investing is highest among younger women:

- 40% of women aged 18-29 want or plan to start investing, the highest of any age bracket.

- 32% of women aged 30-44 share this intent, while interest drops significantly to just 13% for those 45 and older.

- Conversely, women 45+, who are closest to retirement age, are the most likely to already be active investors (40%).

While a plurality of women overall (43%) remains uninvested and uninterested, this near-term interest, particularly among younger cohorts, suggests that the drive for financial autonomy is beginning to outweigh the barriers of cost, risk, and the literacy gap noted above.

5. Cryptocurrency has a long way to go to appeal to prospective women investors, though trust is rising.

Much like the Gen Pop, trust in crypto remains a major sticking point, with 69% of women reporting they have little to no trust in this type of investment. However, this is a significant improvement from the 81% distrust level recorded in 2023, suggesting an increasing openness to digital assets. This shift hasn’t moved the needle on participation just yet; crypto investing experience among women holds steady at 17%, while intent to invest has nudged up only a single point from last year to 12%.

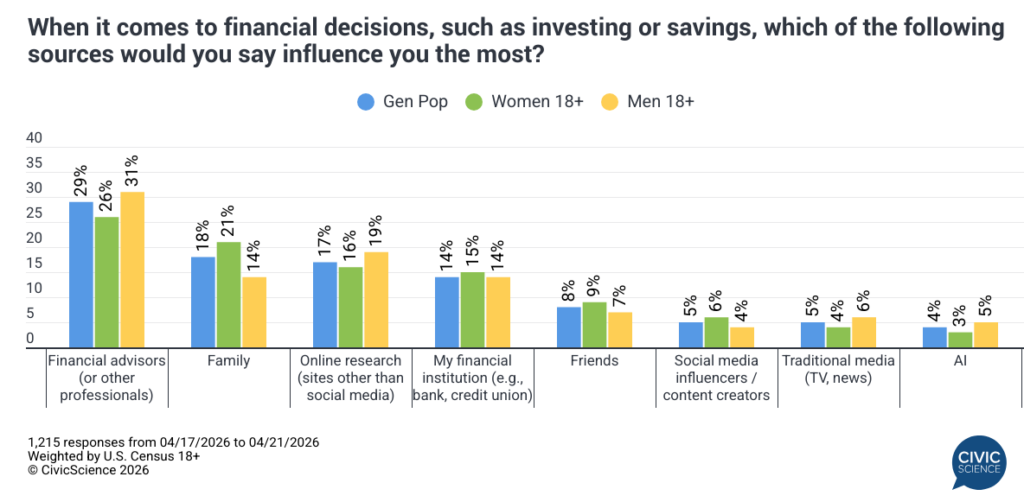

6. Family and professional advisors are the most trusted sources for women when navigating financial decisions.

Among the 71% of women who cite an external influence, a figure consistent among the Gen Pop and men, personal and professional networks far outweigh digital trends. While financial advisors remain the top source of guidance (26%), women are significantly more likely than men to turn to family members (21% vs. 14%) for financial direction. This 50% increase over their male counterparts underscores the importance of trusted, personal connections in closing the financial confidence gap. Conversely, emerging tools like AI and influencer content on social media currently have the least impact on women’s decision-making.

Women might not be “okay” in the traditional sense yet, but they aren’t waiting for the economy to settle before making a move. While the hurdles of confidence and capital are real, the surge of interest from younger generations, backed by the trust they place in family and advisors, suggests a shift is underway. It’s less about chasing a trend and more about women deciding that financial ownership is the most reliable way to navigate an uncertain year.