CivicScience has the world’s largest proprietary database of real-time declared intent, allowing brands to activate high-performing advertising that drives up to 80% better performance. See how our partners achieve superior marketing outcomes here.

Having little financial breathing room after essential expenses are paid is a harsh reality for many Americans today. The implications are far-reaching, but one key area affected is the ability (or lack thereof) to set aside money to cover unexpected costs and emergencies.

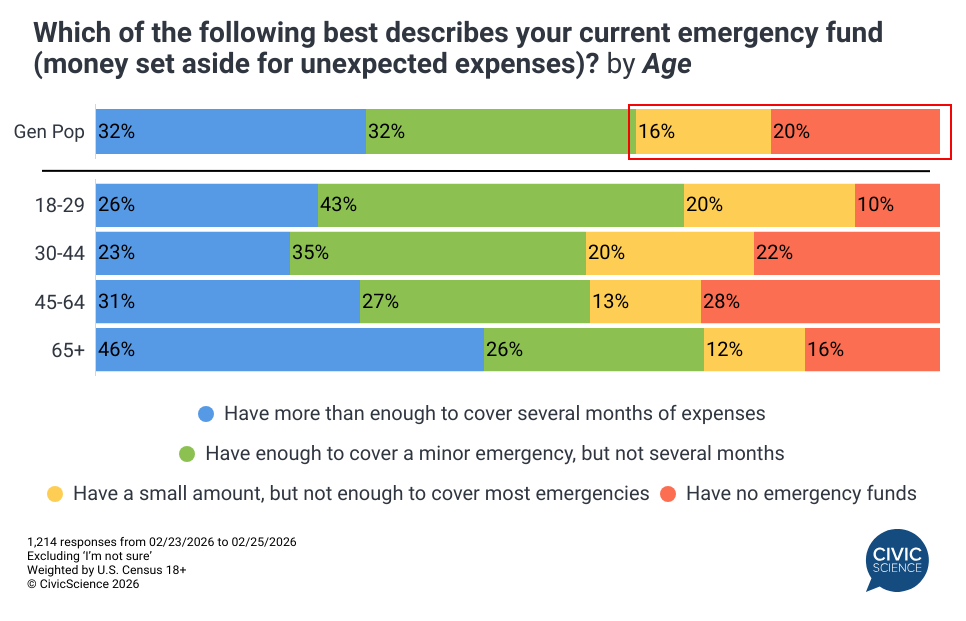

New CivicScience self-reported data among U.S. adults 18+ shows that about one in three adults have ‘more than enough’ savings to cover several months of expenses; however, a higher percentage (36%) report having little to no funds to cover emergencies (excluding those unsure). This disparity is most visible through a generational lens: Those aged 65+ report the highest levels of financial stability, whereas more than 20% of Gen X and Millennials report having no emergency funds at all.

Financial Literacy Compounds the Emergency Savings Divide

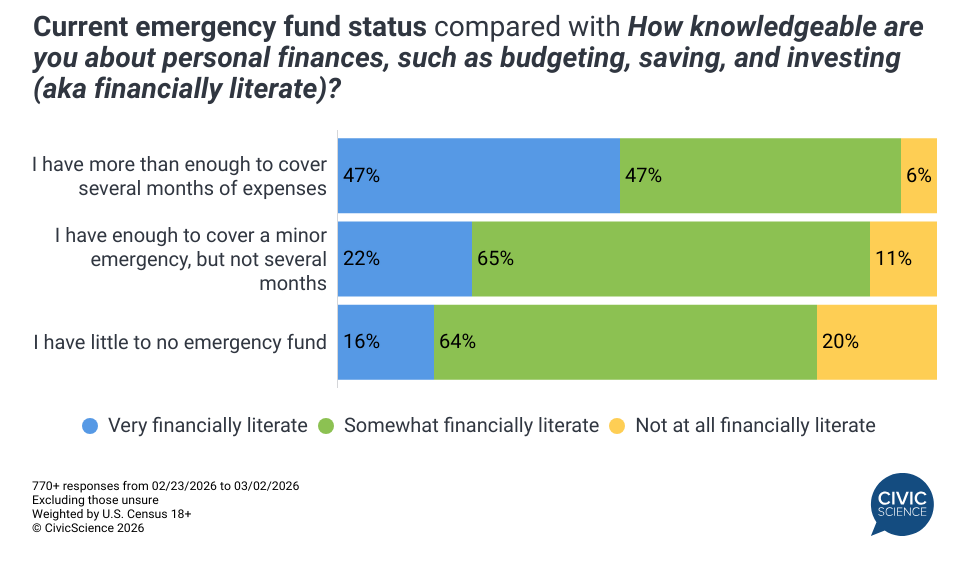

Although living paycheck to paycheck can make it nearly impossible to build up emergency funds, additional data highlights another important factor: Financial literacy. Nearly half (47%) of those who say they have more than enough to cover emergency expenses for several months consider themselves ‘very’ financially literate, 3X higher than those with little to no emergency funds who say the same (16%). Conversely, about one in five (20%) of those with little to no emergency savings tell CivicScience they feel they are ‘not at all’ financially literate, compared to just 6% of those with ample emergency savings. Financial knowledge isn’t a magic fix to instantly close the gap, but in a situation where money is tight, every dollar counts.

Implications for Consumer Spending

When it comes to ways they’re working to improve their current financial situation, Americans who say they have little to no emergency savings are notably less likely than the average American to say they’re cutting back on cable and streaming service spending specifically to improve their financial situation. Binge-watching TV or streaming content is a form of coping with stress for many Americans, including among those with little to no emergency savings, so it makes sense they are less willing to cut media spend. Instead, they’re more likely than the Gen Pop to prioritize reducing what they spend on non-essential groceries.

Additionally, amid the ongoing tax season, those with little to no emergency funds are six points more likely than average to say they’re using their expected tax refund to pay off debt (33%). However, they also outrank Gen Pop in their plans to use their refunds to go shopping by 3 points (11% to 8%, respectively), suggesting that spending among this audience is cautious yet intentional.

Where Americans Turn if an Emergency Happens

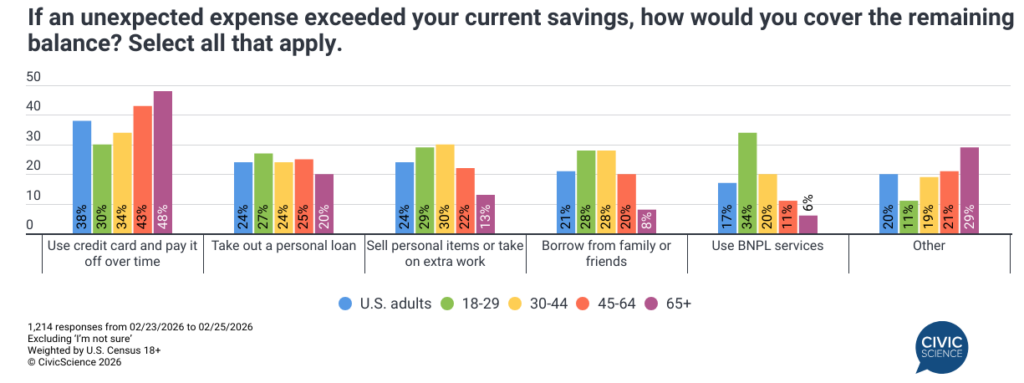

When savings fall short, many Americans lack a structured contingency plan. More than one in four U.S. adults tells CivicScience they have no plan for handling an unexpected expense that exceeds their current savings balance. Among those who do have a plan, credit cards, personal loans, and taking on extra work are the primary fallback options. Gen Z and Millennials are much more likely to turn to loved ones, while Gen Z specifically is more likely to say they would use Buy Now, Pay Later services.

How Much is Enough?

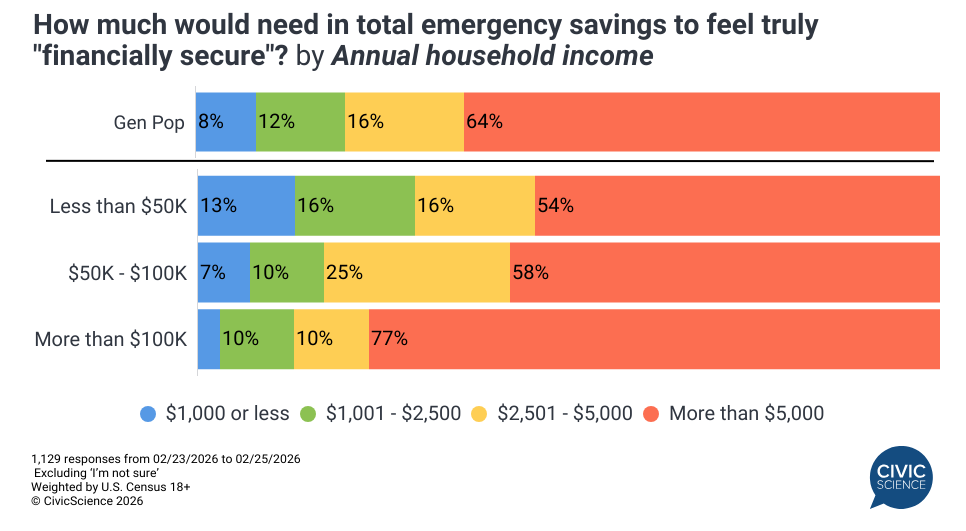

The psychological threshold for “feeling secure” varies, but the consensus points toward a high bar for stability. Regardless of their current income, a majority of U.S. adults believe they would need more than $5,000 in savings to feel safe in the event of an expensive emergency. However, expectations differ drastically among lower-income households (earning less than $50,000); nearly 30% of this group feels they would need $2,500 or less on hand.

For those with little cushion, spending decisions are already deliberate — but when an unexpected expense lands, the most accessible fallbacks can risk compounding financial stress rather than relieving it. Across generations and income brackets, the data reflect a consistent tension between making ends meet today and building stability for tomorrow.