CivicScience has the world’s largest proprietary database of real-time declared intent, allowing brands to activate high-performing advertising that drives up to 80% better performance. See how our partners achieve superior marketing outcomes here.

From JPMorgan signaling growing competition in blockchain and digital assets to ongoing debates in Washington over crypto legislation like the proposed CLARITY Act, 2026 is shaping up to be a pivotal year for cryptocurrency.

According to ongoing CivicScience tracking, 22% of U.S. adults 18+ now report having experience investing in crypto, while intent to invest stands at 12% – both relatively consistent with 2025. But that stability masks a more complicated reality: while overall interest has leveled off, trust remains a significant barrier. Sixty-five percent say they have little to no trust in crypto, with just 9% expressing high trust and 26% moderate trust.

As the industry evolves, CivicScience data shows how consumer perceptions of crypto are changing and where key gaps remain.

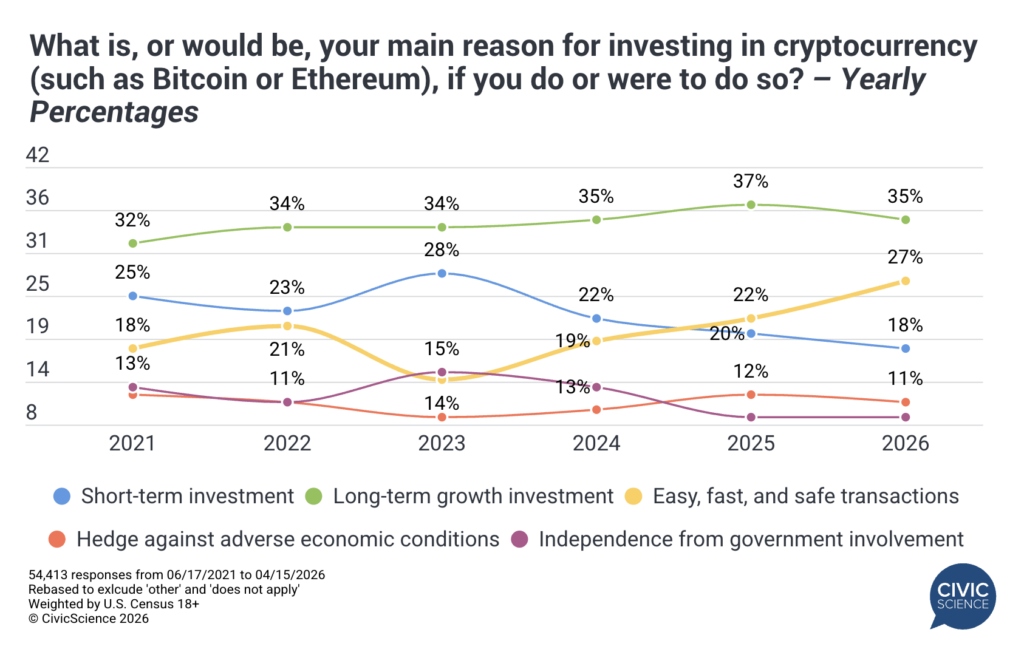

1. Crypto’s Appeal Is Becoming More About the Experience

Long-term growth remains the primary reason consumers currently invest or would be interested in investing in crypto, but that figure has held relatively flat, suggesting its core financial appeal hasn’t strengthened. What is gaining momentum, however, is how people perceive the crypto experience. The share of consumers who say it’s an ‘easy, fun, and safe’ transaction has nearly doubled since 2023, rising from 14% to 27%, and has become the second most popular driver of crypto investing (excluding ‘other’ and ‘does not apply’).

At the same time, interest in short-term investing continues to decline, signaling a potential move away from speculation. Other motivations, such as hedging against adverse economic conditions or seeking independence from government systems, remain steady at around 10%.

For consumers with experience or interest, it’s clear that crypto is no longer viewed solely as an investment vehicle; its perceived ease of use is becoming an increasingly important part of its appeal.

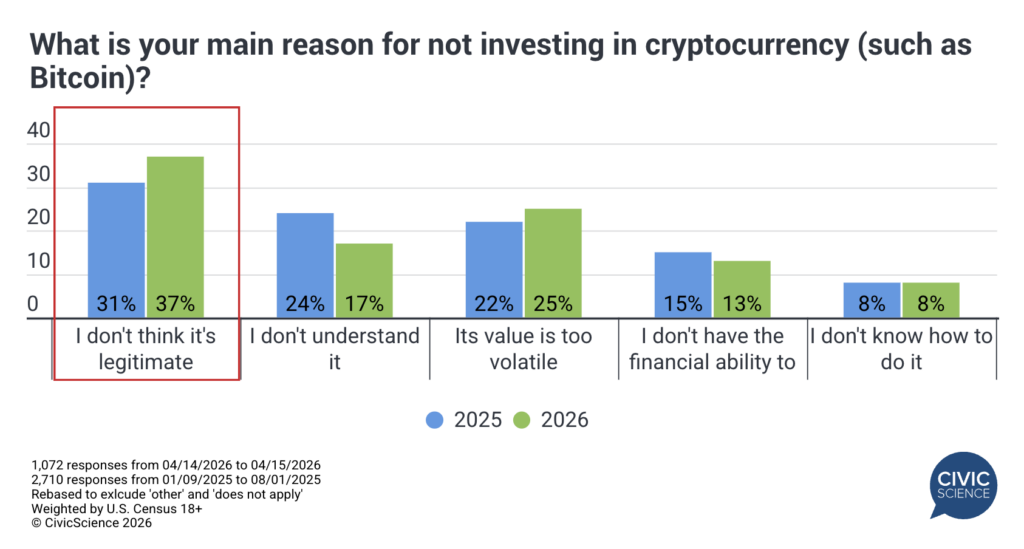

2. At the Same Time, Legitimacy and Volatility Concerns Grow

Even as overall trust in crypto remains low, the reasons behind that skepticism are shifting. The share of U.S. adults who say they don’t invest because they don’t believe crypto is legitimate has increased by nearly 20% in the past year alone, cementing its place as the leading barrier and aligning with the broader trust gap. Concerns about volatility rose three points since 2025, now ranking as the second-most cited reason—surpassing those who say they don’t understand it.

Meanwhile, other barriers, such as not knowing how to invest or lacking the financial means, have remained relatively unchanged and rank among the least common reasons. The challenge is no longer education – it’s credibility.

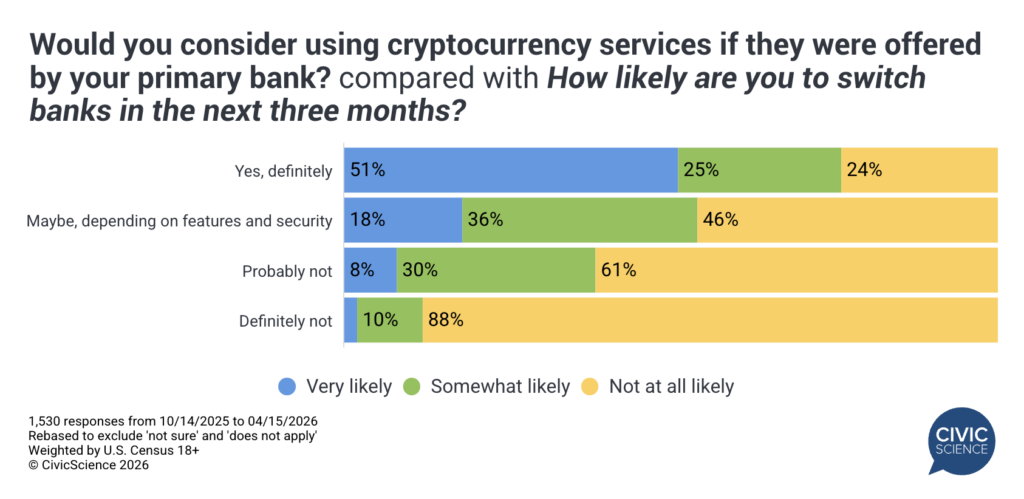

3. Crypto Could Drive Bank Switching Despite Niche Interest

As traditional financial institutions begin to explore crypto offerings, they may play a key role in shaping future adoption. CivicScience data shows that 12% of U.S. adults would ‘definitely’ use crypto services offered by their bank, while another 23% are open to them depending on security – both figures are consistent with interest reported in Q4 2025. However, a majority (65%) remain uninterested.

Interest is highest among Gen Z adults aged 18-29 and those earning under $100K, likely reflecting greater openness to new financial tools among younger consumers. Notably, among those who say they would strongly consider using a bank offering crypto services, 51% report being ‘very’ likely to switch banks in the next three months. This suggests that while overall interest remains limited, crypto could play a key role in driving switching behavior, particularly among younger consumers.

As developments across the crypto landscape continue in 2026, its path forward with consumers remains uncertain. As financial institutions expand their involvement and regulatory frameworks begin to take shape, the real question is whether the industry can close the gap between interest and trust. Until then, continued developments may not be enough to drive widespread consumer adoption.