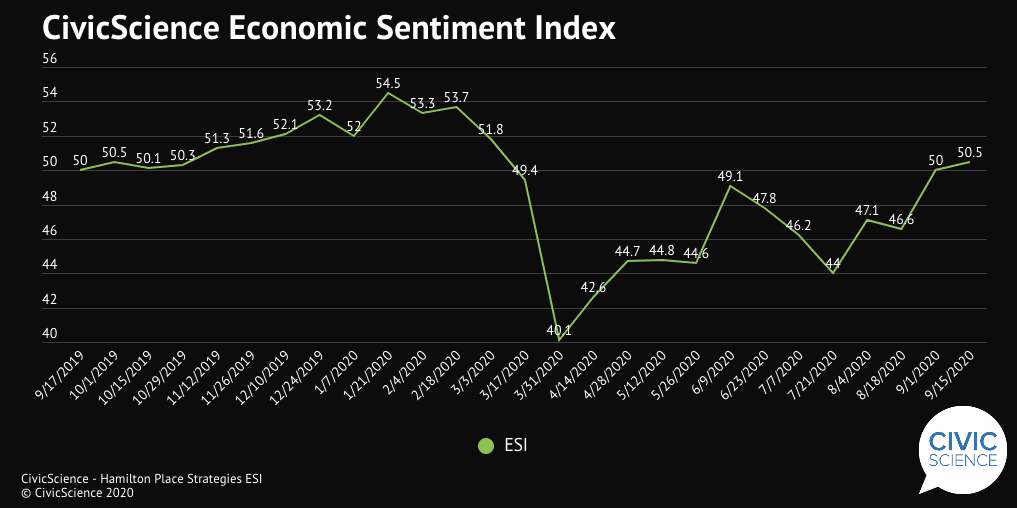

It goes without saying that the HPS-CivicScience Economic Sentiment Index (ESI), a “living” index that measures U.S. adults’ expectations for the economy going forward, as well as their feelings about current conditions for major purchases, has been somewhat of a rollercoaster over the past six months.

The overall ESI, which is measured every two weeks, has looked like this over the past year.

From September of 2019 into the new year of pre-pandemic 2020, things were pretty stable, if not rising. It took a nosedive, of course, beginning in early March, and fully plummeted by the end of that month. Things have somewhat bounced back in early June, and then again starting in early August. Time will tell what the recent beginnings of another case surge will bring, but more on that later.

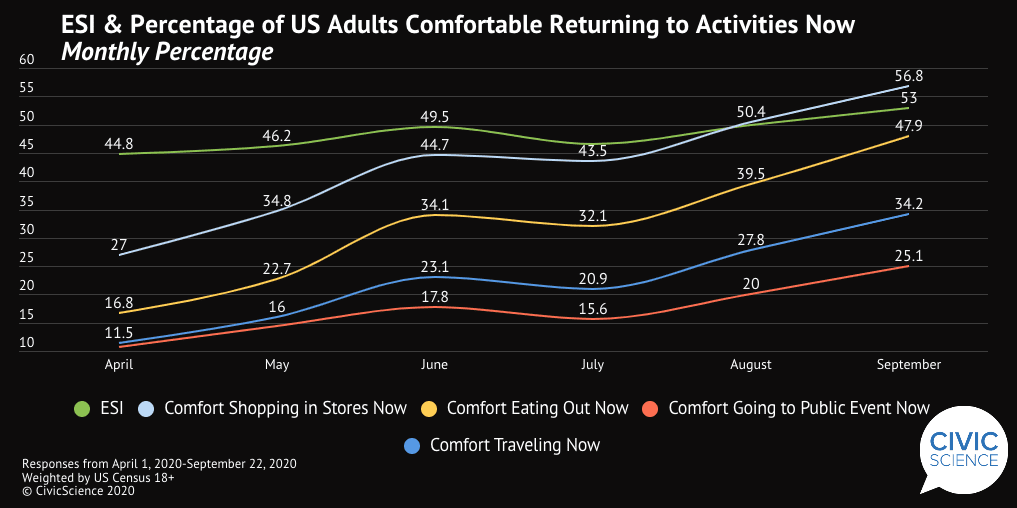

Another wild ride (hope you’re strapped in) is consumer’s willingness (read: comfort level) to return to many normal activities that were just everyday normal events prior to March. Again, no surprise there.

Dining at restaurants, going out to major public events, shopping at stores, and comfort taking a trip, have all been up and down. However, when comparing people who self-report being comfortable doing those four major things now with the overall ESI, we see a clear correlation.

The below data is the overall monthly percentage of the ESI (a different time-grain than above) and the percentage of U.S. adults comfortable with a return to activities now. As you can see, one drives the other, so to speak. A better way of thinking about it is: the higher percentage of people who say they are comfortable returning to restaurants, stores, and the like now, the higher the ESI seems to tick. Thus, the higher the overall consumer confidence is in the future economy.

In full, the ESI score (shown above in green) measures the following indices, asking Americans about their confidence in:

-Buying a new home

-Their personal financial situation

-Finding a new job

-Major purchase (like a car)

-U.S. economy

Slowly but surely, increased confidence in all of these categories has driven the ESI up to some extent.

We dig into one example, restaurant dining, of which the percentage of Americans who say they are now ready to wine and dine out hit a new pandemic high of 50% last week. Those who said over the past two months that they were comfortable dining at a restaurant over-index in thinking the U.S. economy will get better six months from now.

The most important consideration we’ve seen to date that indicates comfort returning to pre-pandemic activities, like dining out for one, is that the wealthier you are, the more likely you are to be okay with getting back to partaking.

This is the case overall with the ESI, it appears. Rich Americans, with a whole lot less to lose and likely who have not lost much as a result of the pandemic, are driving the whole ESI up as a result of their own comfort returning to their old day-to-day.

Overall, the correlation between the ESI’s path over the past six months and consumer comfort getting back to normal activities is evident so far. But what about if cases surge as the weather gets colder and flu season is upon us? Will Americans change their tune when it comes to comfort levels if the ESI goes down? CivicScience will continue to track this multi-timeview report in the ESI’s off weeks.