Things are teetering.

That sounds grimmer than I intended. It could certainly tip in a positive direction. Or not. I just don’t know.

This isn’t so much about the economy, inflation, the election, or the shit-show in the Middle East. It’s all of it – and how it’s weighing on our collective psyche, however consciously.

Over the years, I’ve peppered you with a consistent cadence of our three main consumer indices: Economic Sentiment (ESI), Consumer Financial Health (CFHI), and Emotional Well-Being (WBI). I’ve never really explained why.

The ESI was our flagship, originally built to predict the Michigan Consumer Sentiment Index, which can often move Wall St. The ESI, like Michigan, tells us how people feel about the U.S. economy, job market, housing market, and other forward-looking factors. We noticed, however, as I’ve written and spoken about ad nauseam, that beginning in 2016 the ESI became as much a measure of political attitudes as economic ones. That doesn’t make it meaningless, on the contrary, only different.

Then we began developing the CFHI, which focuses on consumers’ personal financial outlooks – income, debt, savings, and the like. It’s proved to be more immune to politics and news cycles (though not entirely). Meanwhile, the individual components gave us a better view of specific sub-groups and their spending capacity.

The WBI came a little later – fortuitously prior to COVID – after which, tracking people’s feelings of hope, fear, and other emotions helped explain unintuitive spending, workforce, and health behaviors in the face of inflationary headwinds. It rounded out our view.

Together, these indices are harmonious. The CFHI is the most correlative and, in some cases, predictive of overall spending, especially services categories. The ESI is particularly correlated with spending on durable goods. The WBI aligns with the utilization of health services and spending on a mix of other goods and services.

None of them paint a vivid picture of the future right now.

Broadly, things aren’t bad or good – that would require a consistent trend in one direction or the other. What’s concerning is the volatility. All three of our indices, respectively, are almost exactly where they were at the end of January, masking a flurry of news-driven ups and downs since.

Without a coherent pattern or clear tipping point (like an election), it’s impossible to know where things are headed. I feel it. The companies we work with feel it. And the average person feels it.

As much as I wish I could predict the future for you, I can’t. Nobody can. All I can promise is we’ll be the first ones to know when the fog lifts.

And you’ll be the second to know.

Here’s what we’re seeing:

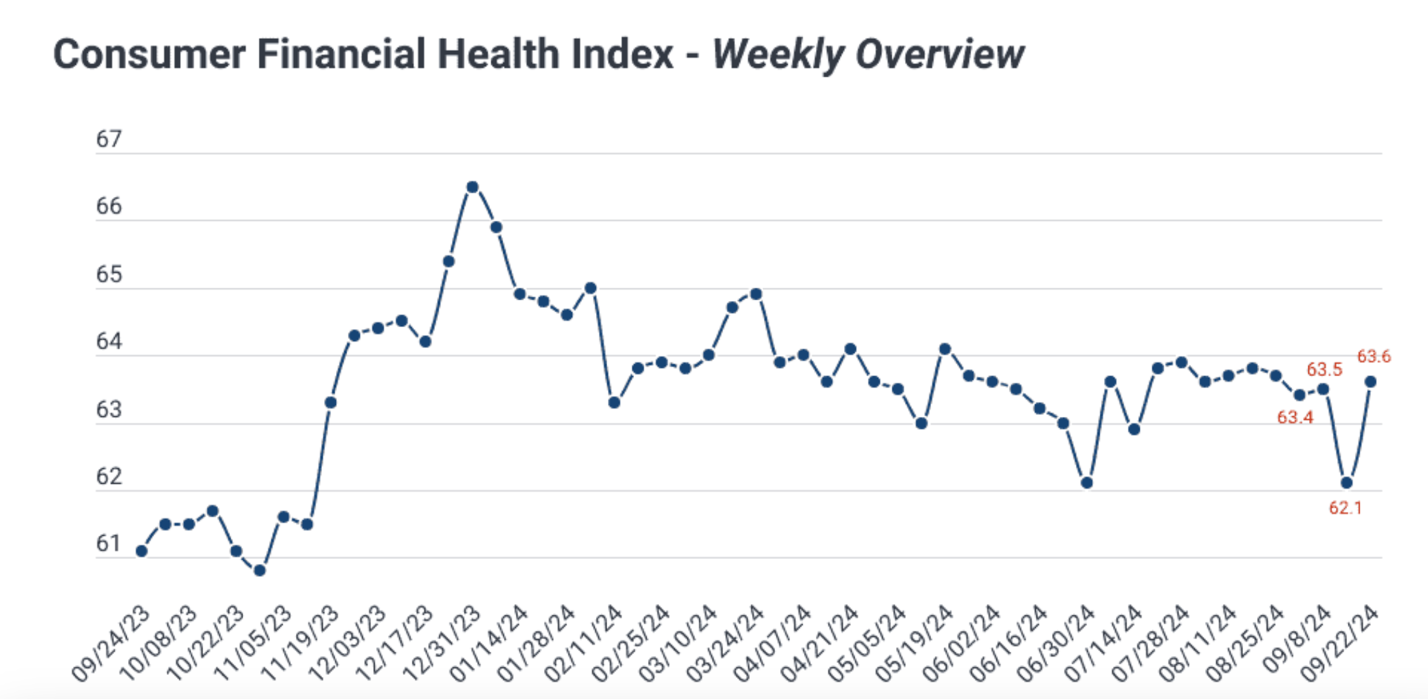

On that note, consumer financial health spiked over the past two weeks, simply making back the losses it suffered the two weeks prior. Our latest CFHI was published this week. The good news is two-fold: 1) People are considerably more positive than they were this time last year and 2) Debt concerns have remained remarkably steady. The bad news is that our collective outlook around savings and investments is going south. It’s a hodgepodge and – again – difficult to find a predictive through-line.

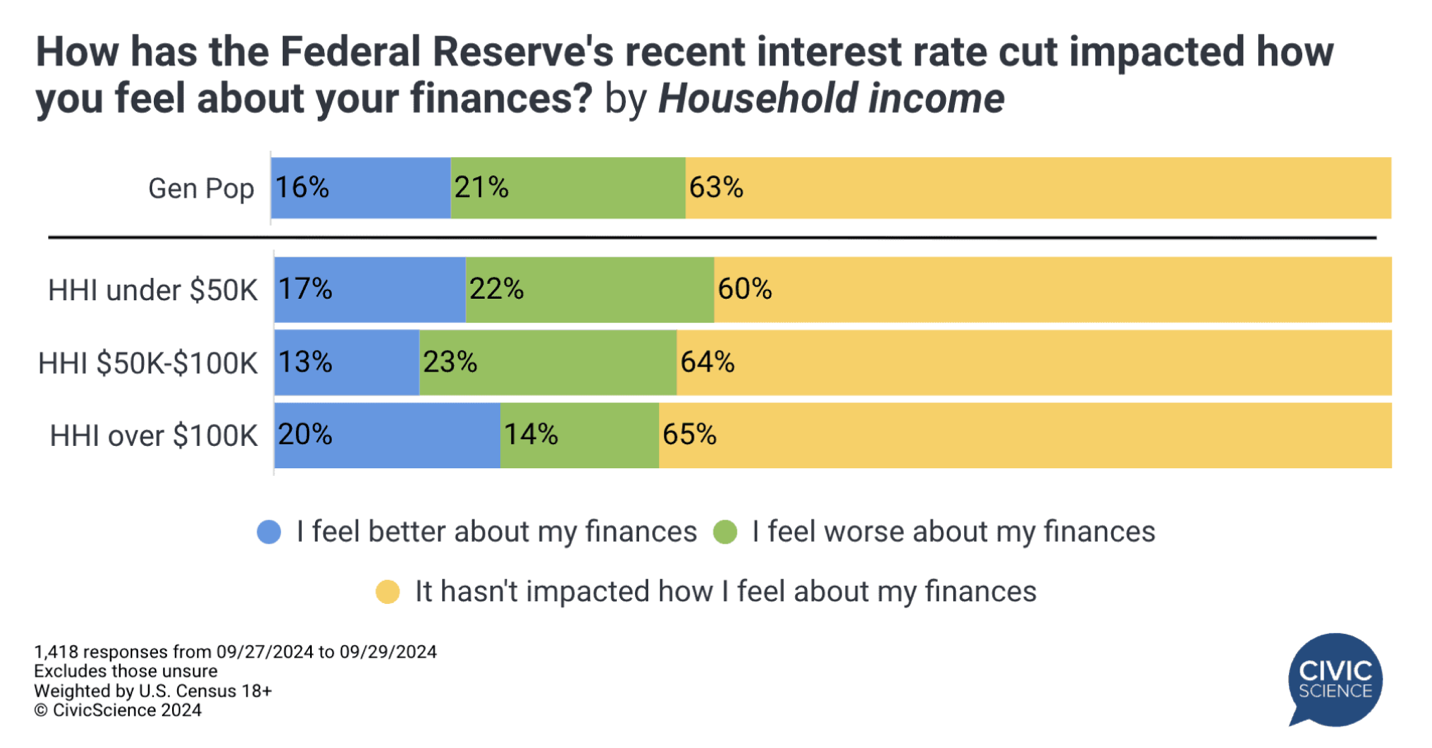

One thing that doesn’t seem to have impacted consumers’ financial outlook was the recent rate cut. If anything, highest-income Americans aside, more U.S. adults say they feel worse about their finances after the move, while a clear majority say it made no difference. In the end, it tells me that most people range somewhere between disaffected by interest rates to oblivious about their impact on the economy. One key point from this study, though, is that Gen Z now seems more emboldened to make a major purchase and apply for a new credit card going into the holidays. I guess that’s good – in the short term.

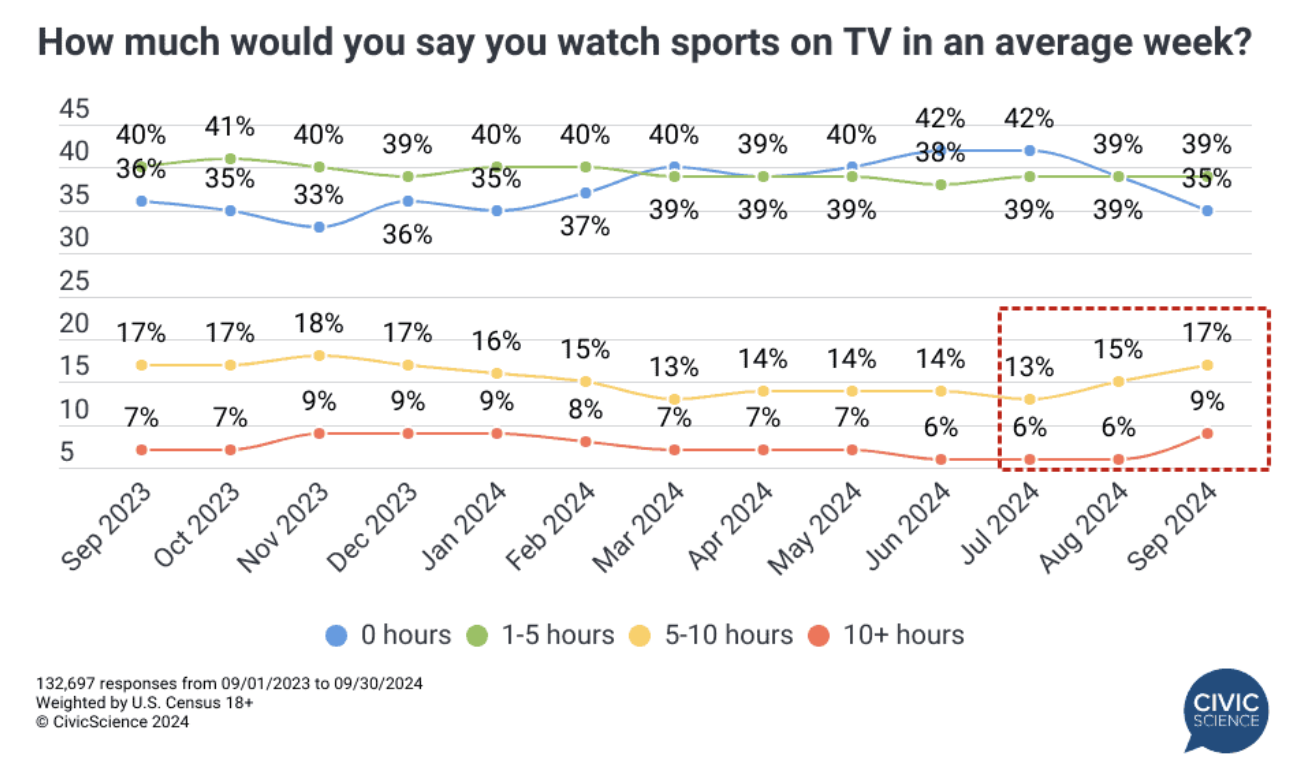

Interest in sports is back to levels we haven’t seen since before the pandemic. Per usual, excitement about sports is accelerating as the NFL season, baseball playoffs, and the impending return of the NBA and NHL converge (new to the party is the heightened interest in the WNBA playoffs). In sum, enthusiasm is the highest we’ve seen in five years, potentially because people welcome the escape. One loser in this trend could be game ticket sales, as consumers report greater concern over costs. The winners, on the other hand, will be the sports streaming services, particularly ESPN+ and Amazon Prime. They’re cheaper, of course, and you don’t have to wait in line for the bathroom.

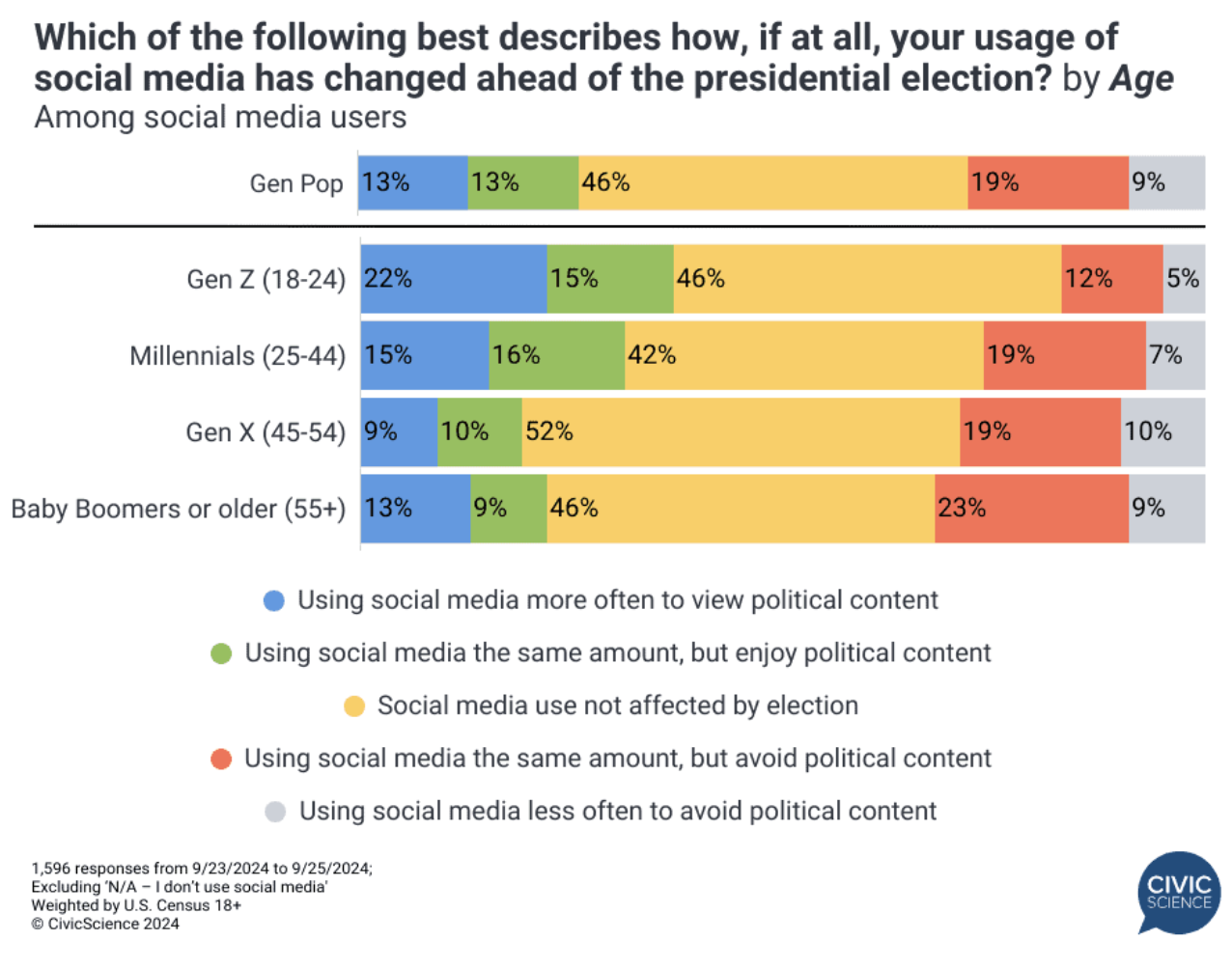

Gen X is sick of your political posts. In our 3 Things to Know this week, we looked at how the election season maelstrom is affecting Americans’ usage of social media. Overall, the general population is slightly more likely to be avoiding political content – or social media altogether – than those who are leaning in for it. There are big age splits, though, as Gen Z is upping their social media game to find politics at over 2:1. At the other end of the spectrum is Gen X, because, well, we’re tired. In other news, we studied the evolving motivations of consumers when it comes to replacing their cell phones and how promotional events will lure shoppers into malls this holiday season.

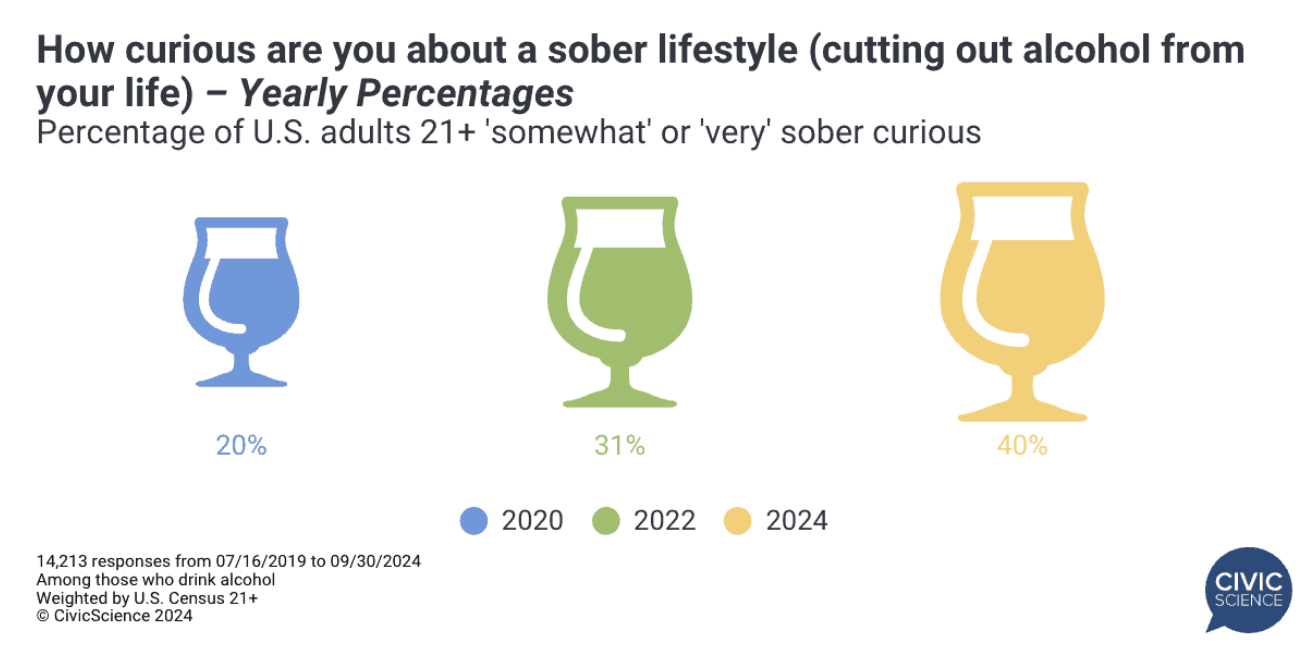

We didn’t study it, but I’m guessing the people participating in Sober October aren’t paying close attention to politics. Although maybe these people are just preserving their livers for a huge bender while they anxiously watch the election results roll in. In any event, we found in this study further big signs of trouble for the alcohol industry, as “sober curiosity” has climbed by a full 2X since 2020. Especially among younger drinking-age consumers, cannabis and non-alcoholic beverages continue to fill the void.

More awesomeness from the InsightStore this week:

- The trend of self-gifting seems to be slowing heading toward Christmas;

- Introverts can now use the economy as an excuse for not socializing;

- 83% of Americans eat Mexican food at least monthly and other National Taco Day insights.

The most popular questions this week:

Are you a fan of horror films?

How often do you eat sauerkraut?

Answer Key: Yes, among friends too; Literally never; Yeah; Not even a little; Every time it’s offered to me.

Hoping you’re well.

JD