Adjustable rate mortgages (ARMs) are a lending product that has appealed to many prospective homebuyers over the years. ARMs are typically a 30-year loan that begins at an initial fixed rate – lower than current market rates – but increases after a set period of time. According to financial experts, ARMs are risky but can be a wise choice for some homebuyers, depending on their financial status and financial goals.

In the current market, ARMs can support homebuyers who are struggling to afford interest rates as they are right now (over 7%). Starting at a lower rate could mean certain consumers are able to purchase the home they need while also having the time to build financial stability for future rate increases. What’s clear about ARMs is that they are unpredictable and consumers have to weigh risk against personal financial goals.

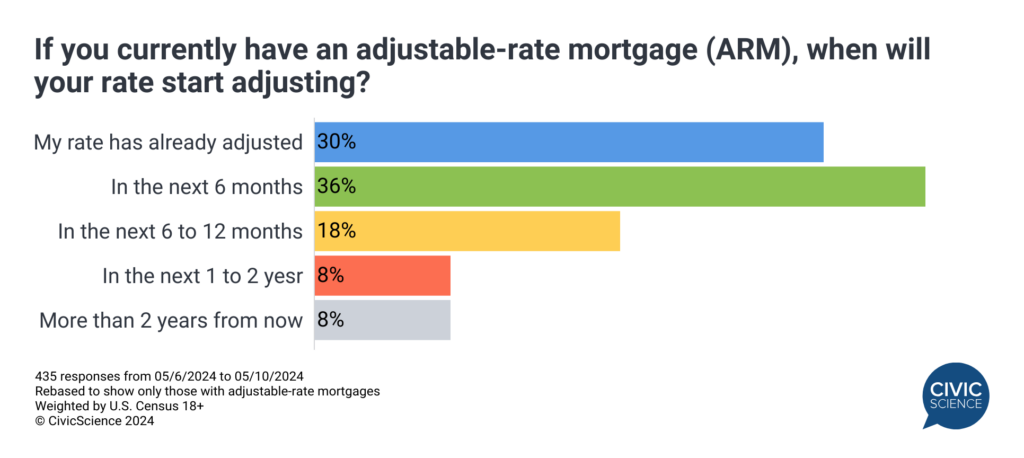

CivicScience data show adjustable-rate mortgages are most often utilized by wealthier Americans, those with an annual salary of $100K or more, who want to buy more expensive properties or are more likely to be able to afford an increased monthly payment when the time comes. ARMs are also most common among homebuyers under 35, indicating recent lending either just before, during, or post COVID. Fourteen percent of homeowners have adjustable mortgages, and 54% of ARM holders say they will experience an increase within the next 12 months.

Join the Conversation: Do you personally prefer to take out an adjustable-rate mortgage or a fixed-rate mortgage when buying a home?

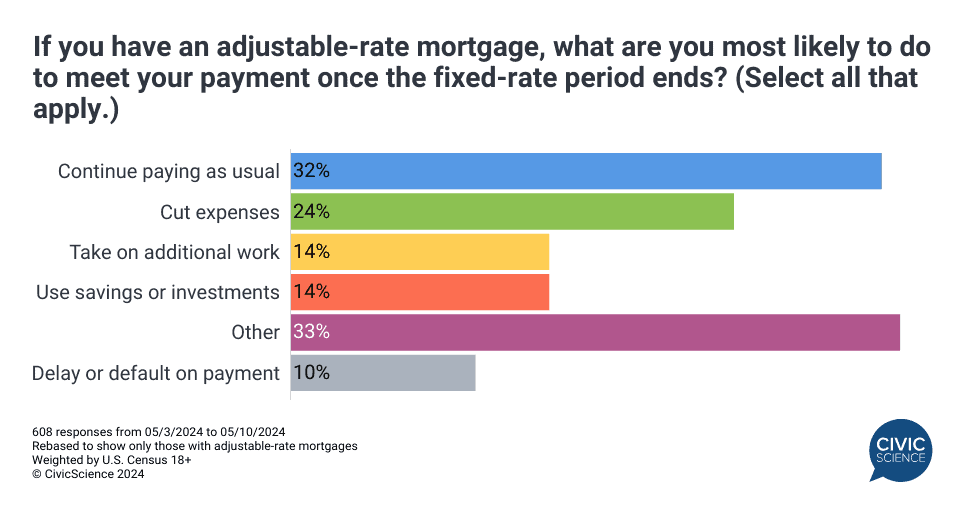

This could be a dicey 12 months for homeowners awaiting a rate hike. While close to one-third of ARM consumers will simply continue to pay as usual once their mortgage rate adjusts, roughly one-quarter plan to cut current expenses to afford the adjustment. And 14% will either take on additional work or use savings or investments to cover the larger payment. People with adjustable-rate mortgages are also more likely to report extreme levels of stress, and expect to have significantly more debt within the next six months.

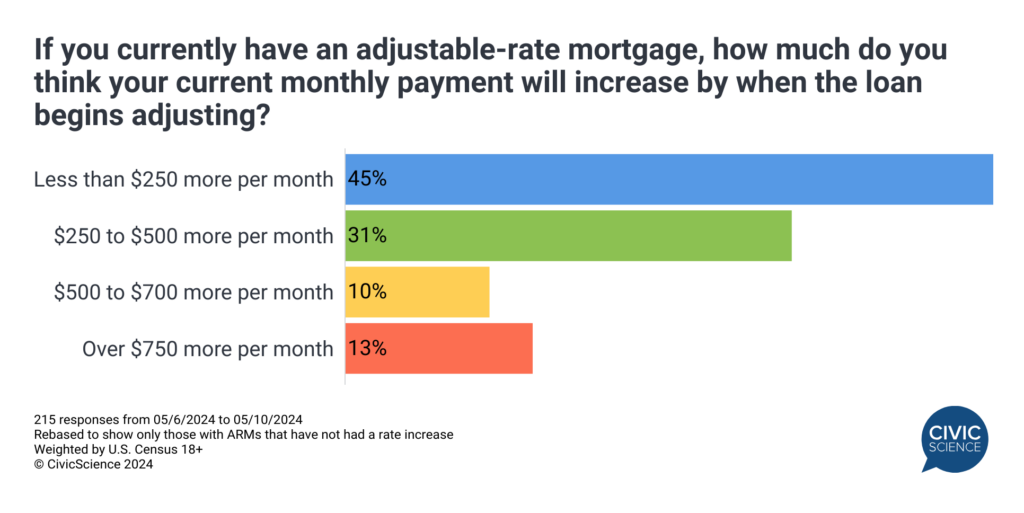

Forty-five percent of those who are still awaiting a rate hike say they don’t anticipate an increased dollar amount above $250 per month. Thirty-one percent are expecting to see a rate increase between $250 and $500 per month. A startling 8% say they anticipate an increase of $750 or more per month, which adds color to the fact that 10% of ARM homeowners plan to simply default on the loan when payments increase.

What Do You Think: Will mortgage rates drop this summer?

CivicScience polling paints a picture of the real estate market that doesn’t look great for many homeowners and prospective buyers. Lending rates are still extremely high and no one seems to know when they will start to come down again. Bloomberg identified that in some instances an adjustable mortgage will double when the fixed period ends, and not everyone will be ready for that. Those considering such a loan are weighing the risks.

Attitudes change before behaviors do. To learn how the CivicScience InsightStore helps clients track shifting consumer attitudes toward the housing market and industries across the board, get in touch.