The Gist: Millennials prefer cash and debit cards much more over credit, and it likely has to do with student loans and the experience of older generations.

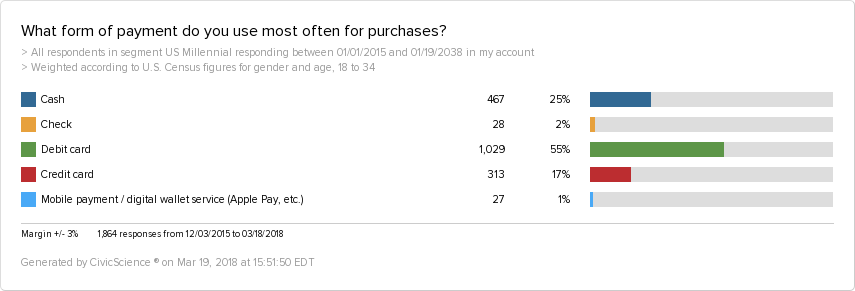

Millennials have been blamed for the demise of everything from napkins to retail, but there’s one institution that the generation holds onto–cash. Who should be concerned? Credit card companies.

While the germ averse hold out hope for the end of cash in favor of credit, debit or mobile payment, a surprising amount of Millennials pay primarily using bills.

Unsurprisingly, this demographic isn’t writing checks, but it’s interesting to note how few of them are adopting tech, such as Apple Pay, to make transactions. Most rely on debit, but cash isn’t far behind.

In the past two years, we’ve seen Millennials using cash more frequently. In Q4 2017, Millennials were more likely to pay with cash more than any other form of payment. Debit has been on a slow decline, while cash has, for the most part, risen. Credit cards, while fairly steady, have seen a decline while cash rises.

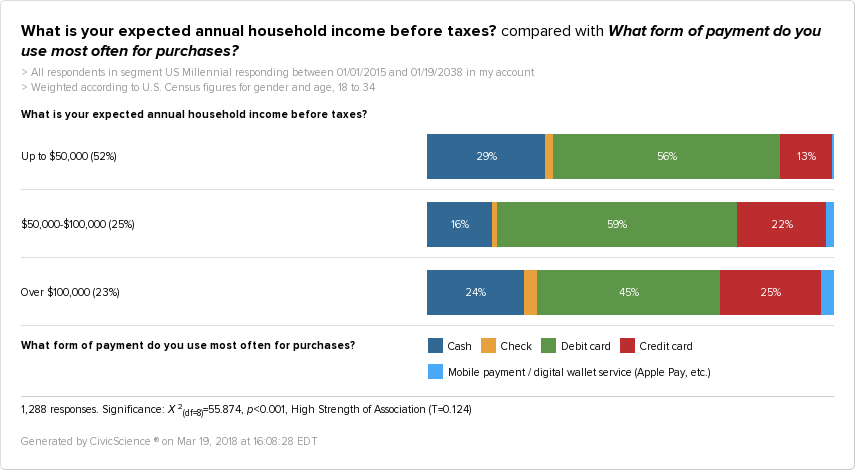

Why might this be? We dove into the income of Millennials and got some (but not all) of the answers.

Credit card usage amongst this age group is tied to income. However, we can’t say the same about cash. High and lower earners are more likely to use cash than mid-range earners. It’s a head-scratcher.

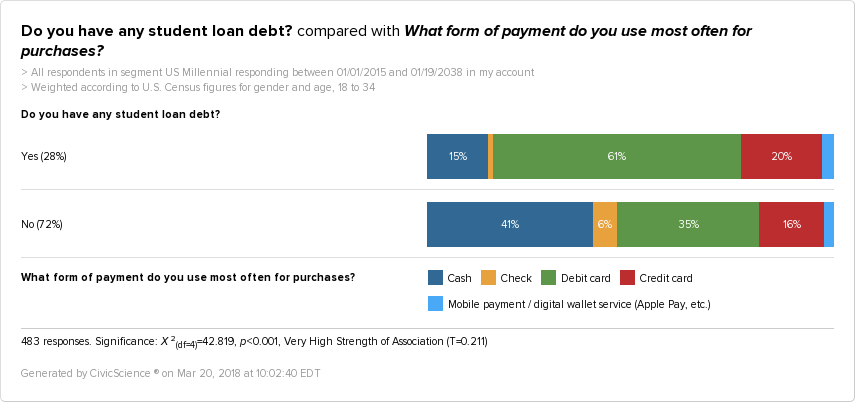

Could cash usage, or debit usage be connected to debt? If we know anything, it’s that Millennials are swimming in student loan debt.

It’s clear from this that there’s a connection between Millennial debt and debit card usage. Millennials with student loan debt are twice more likely to use debit cards than Millennials without student loans.

It’s not hard to link debit card usage among Millennials and money management. Millennial debit card users are more likely to frequently bank online, but are half as likely to self-identify as “managing their money well.” This group is saddled with student loans, monitoring their spending, but still, say they aren’t managing their money well.

Millennial credit card users, on the other hand, are quite the opposite. They are more likely to be diligent savers, manage their money very well, and carefully monitor their retirement savings. Millennial credit card users present as financially savvy, and their lack of debt proves it.

Compare that to 46% of Gen Xers and 40% of Baby Boomers who have credit card debt, and an interesting narrative emerges.

Millennials grew up seeing credit cards as a negative, especially the burden credit card debt, on parents and relatives. I remember multiple “very special episodes” of sitcom television dedicated to the perils of overspending on credit cards. Maybe that hokey television paid off–Millennials who do use credit cards are more financially literate than their peers. The majority of Millennials use cash and debit cards, perhaps in a move to prevent spending beyond their means.

Only time will be able to tell if financial stability of Millennials will breed higher credit card usage. Right now, it looks like the credit card industry could suffer from lack of Millennial engagement. But cold hard cash? That’s not going anywhere unless Millennials say so.