A recession is coming.

There, I said it.

Two years ago, when mainstream economists, the press, and Jamie Dimon incessantly rang alarm bells about an imminent recession, we were among the most outspoken naysayers. The consumer – whose spending accounts for 70+% of the U.S. economy – was too flush with cash, too optimistic, too resilient. Our data was incontrovertible.

If we trusted that data enough to stick our necks out then, we have to do it now.

To be fair, a downturn is inevitable…eventually. Since America was birthed, we’ve never gone a decade without a bona fide recession – until now. We’re going on 15 years at this point. It can’t continue forever.

But I’m not just betting on a cycle. We told you last fall that if consumers recklessly spent their way through the holidays (they did), they’d crash into a wall of credit card and BNPL debt (they did). Now, they’re cutting back.

The job market is moderating – at best – and inflation remains pesky. Juicy severance packages that blunted the short-term impact of mass corporate layoffs are fading. The techies who jumped into new jobs took them from recent college grads – among whom unemployment is up 50% YoY.

All that led to a downward-revised 1.3% GDP growth in Q1, a number that’s much closer to zero than the 3.4% we saw in Q4 2023. I suspect Q2 will be about the same. From there, it’s a big fat question mark.

Meanwhile, our Economic Sentiment Index has been sliding steadily since January. Sustained dips we’ve seen in the past were tied to a non-linear trigger – COVID, the war in Ukraine, etc. What’s happening now is more systemic, more organic. No single event explains it.

Making matters worse is the uncertainty of the upcoming election. Both sides believe democracy is at stake. At least one-third of the country will be devastated by its outcome. And if I’ve taught you anything over the past eight years, it’s that consumers are acutely impacted by political anxiety. I can’t see how it will be good.

At the same time, companies (and investors) are pouring billions and billions of dollars into AI, most of them with no idea whatsoever how it’s going to make money. It’s a bubble of the highest order, as the inimitable Scott Galloway explained far better than I can.

So yeah, a downturn – hopefully light and brief – is on the horizon, if not by the end of the year, then soon after. Hopefully, I’m wrong.

There’s a first time for everything.

Here’s what we’re seeing:

All that said, consumer confidence had a modest upswing at the end of May. One of our cardinal rules is to never obscure data even when it doesn’t fit a narrative, so I’m obliged to share the following. Over the past two weeks, our Economic Sentiment Index had its first considerable improvement since March. The gains came mostly from increased optimism for finding a job, the metric that has otherwise fallen the most over the past several months. In any event, it’s one reading. I’m not back-pedaling yet…

Because while macroeconomic outlook may have improved, personal financial health went the other direction. Coincidentally, our monthly Consumer Financial Health Index came out this week too, and it paints a picture more aligned with my prologue. Personal savings outlook took the biggest hit, dropping nearly two full points since April. Of our five main indicators, credit outlook is the only one that climbed – perhaps people are dipping into their savings to pay off their credit card bills. Debt outlook remained steady, but still depressed.

People are increasingly concerned about being laid off from their jobs. I swear, I wrote my intro before looking over all the studies we published this week. I don’t mean to beat a dead horse here. But in our 3 Things to Know, we looked at growing worries among U.S. adults as it pertains to their job security. We also found that a large share of Baby Boomers and older Gen Xers expect to need gig work or other supplemental income after they reach retirement from their primary job. In less serious news, we also reported on changing preferences in video games, as players look for more casual, low-stress games.

A near majority of Americans aren’t interested in AI-enhanced online search, as if they have any say in the matter. As Google and others begin enhancing their services with AI-generated search results, people are pretty negative on the idea – those not interested in the capabilities outnumber those who are interested by an even 2-to-1. Part of the problem is that 46% of U.S. adults say they have “no trust at all” in the credibility of AI-generated content. The story changes a bit, however, when it comes to product searches, particularly among those who start their retail searches on Instagram or TikTok.

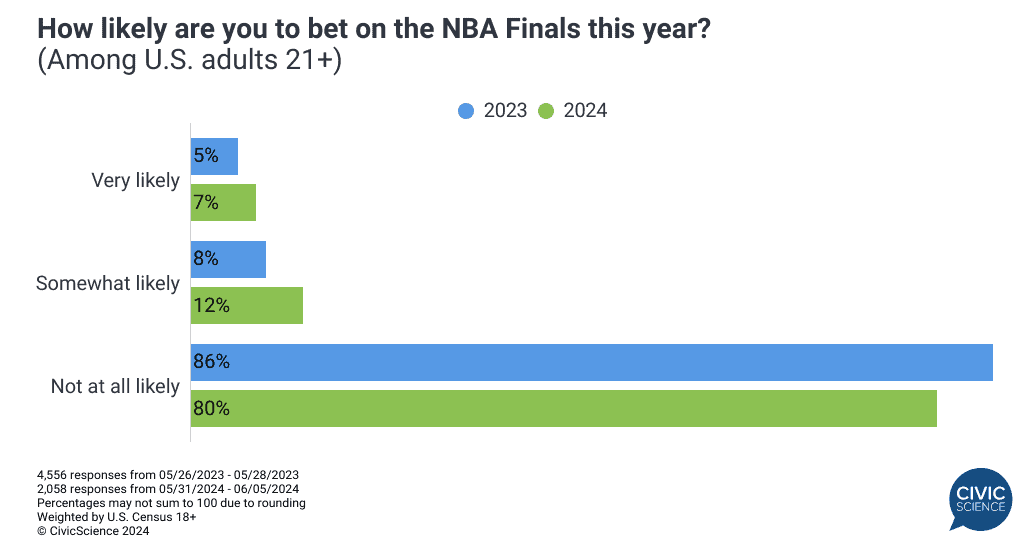

More people plan to bet on the NBA Finals this year. As the Boston Celtics and Dallas Mavericks get underway in the latest championship tilt (go Mavs!), the percentage of Americans who plan to watch was up a single point over last year. Likely bettors, however, climbed over 40% during the same period. A large number of viewers report a likelihood to order food delivery while watching (a good sign for DoorDash, a longtime NBA partner). Notably compared to fans of other pro sports, NBA fans are the most likely to order burgers and chicken sandwiches. Who knew?

More awesomeness from the InsightStore™:

- As Pride Month festivities get rolling, LGBTQ+ attendees are concerned about their personal safety at events;

- The majority of student debt holders still haven’t begun paying down any of their debt;

- Fewer women, more men are wearing makeup than they did two years ago.

The most popular questions this week:

Do you always return your shopping cart to the corral at the grocery store?

Is shared household labor a must in marriage?

How often, if ever, do you check the weather forecast?

Do you prefer bone-in meat when grilling?

Do you consider Pittsburgh to be part of the Midwest?

Answer Key: Yes, because I’m not an asshole; Yes, because I’m not an asshole; Usually multiple times per day; Not really; Yes, definitely.

Hoping you’re well.

JD

Not on the list to receive this email? Sign up here. If you are new to this list, check out our Top Ten to get caught up.