CivicScience has the world’s largest proprietary database of real-time declared intent, allowing brands to activate high-performing advertising that drives up to 80% better performance. See how our partners achieve superior marketing outcomes here.

1. More than 2 in 5 U.S. adults say financial content creators hold at least some influence over their financial decisions, led by YouTubers.

Financial influencers and online creators exert a particularly noteworthy impact on consumers’ personal financial decisions. New self-declared data from CivicScience finds that 41% of U.S. adults report their financial decisions are influenced, at least ‘a little,’ by digital financial creators. Nearly one-quarter (23%) say these “finfluencers” have either a ‘moderate’ or a ‘great deal’ of pull on how they handle their personal finances. This impact is overwhelmingly concentrated among younger consumers: 81% of Gen Z (18-29) and 64% of Millennials (30-44) acknowledge that online financial creators hold some sway over their decisions, compared to a 23% among Gen X (45-54) and a much more negligible impact among those aged 65+ (7%).

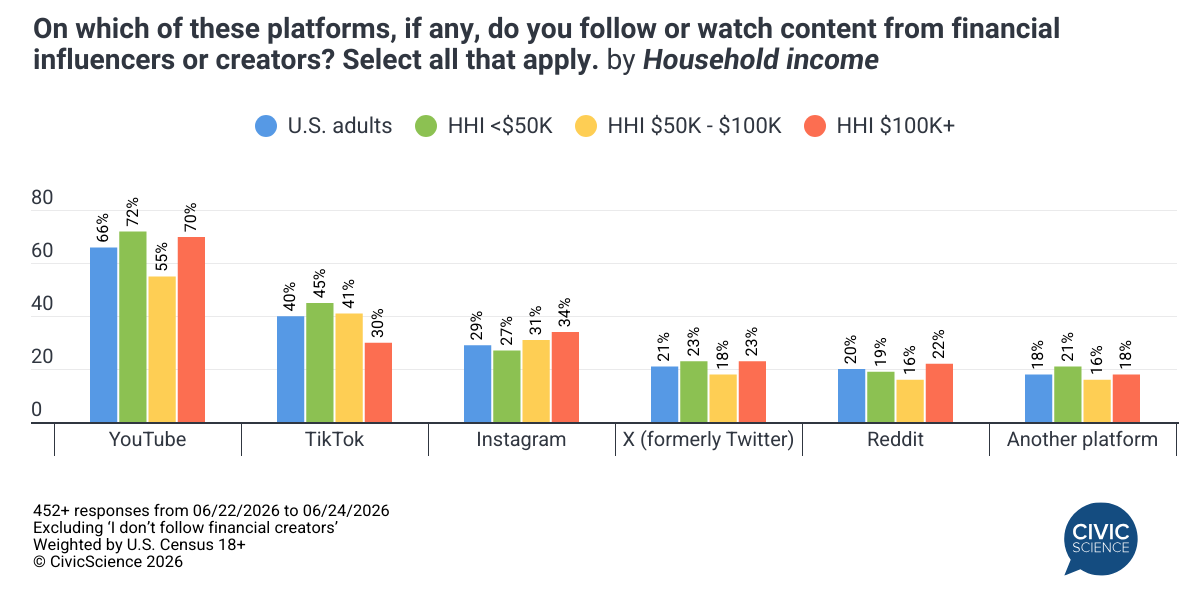

Among consumers who follow financial creators, YouTube is the most common platform, capturing 66% of respondents, followed by TikTok at 40% and Instagram at 29%. However, platform preference shifts noticeably when segmented by household income. Lower-income audiences (HHI <$50K) heavily favor video, short-form entertainment platforms, showing the strongest affinity for content on YouTube (72%) and TikTok (45%). Higher-earning individuals (HHI $100K+) lean more toward polished or discussion-based formats, with the highest usage rates for Instagram (34%), X/Twitter (23%), and Reddit (22%). This suggests that brands looking to partner with financial creators must align their platform choice with the precise income demographic they aim to target.

Take Our Poll: How likely are you to invest in a financial product or service once it is heavily marketed by social media influencers?

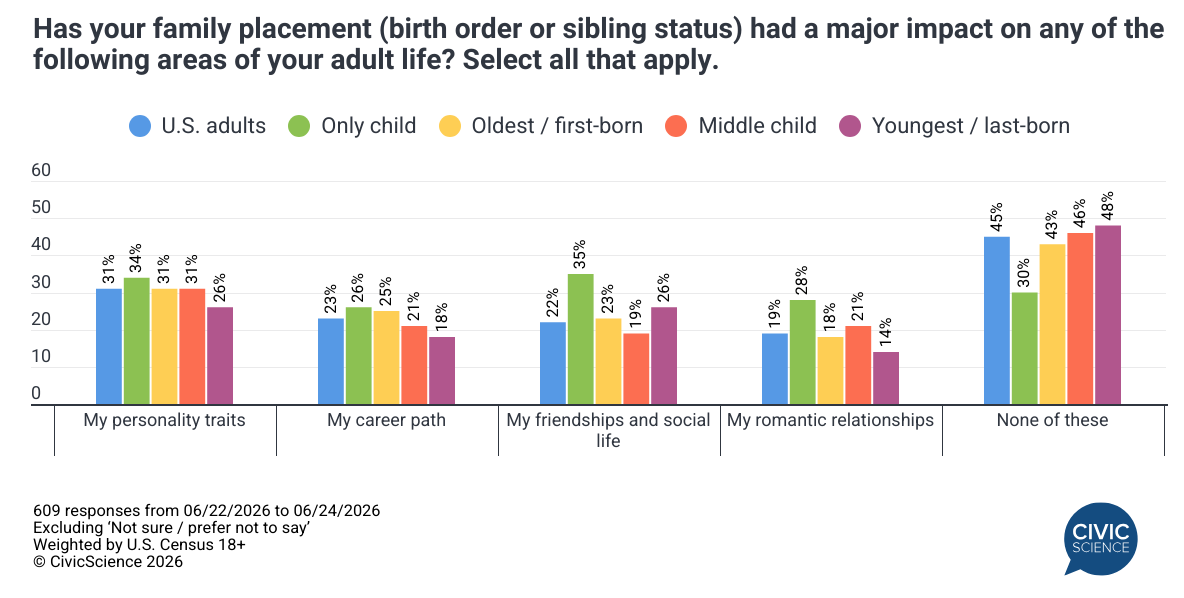

2. A majority believe their birth order and/or sibling status have significantly shaped their adult lives, impacting everything from personality traits to career paths.

When asked if family placement (birth order or sibling status) has altered their adult lives, a majority (55%) agree that it has (excluding those unsure). Personality traits are the most affected area (31%), followed closely by career paths (23%) and friendships (22%). Those who are an “only child” are the most likely to experience downstream effects on their social lives, with 35% reporting a major impact on friendships and 28% on romantic relationships. They also lead in citing impacts on their career paths, with those who are the oldest child following closely behind. Consumers who are the “youngest child/last born” are the least likely to report feeling a major impact in the areas studied.

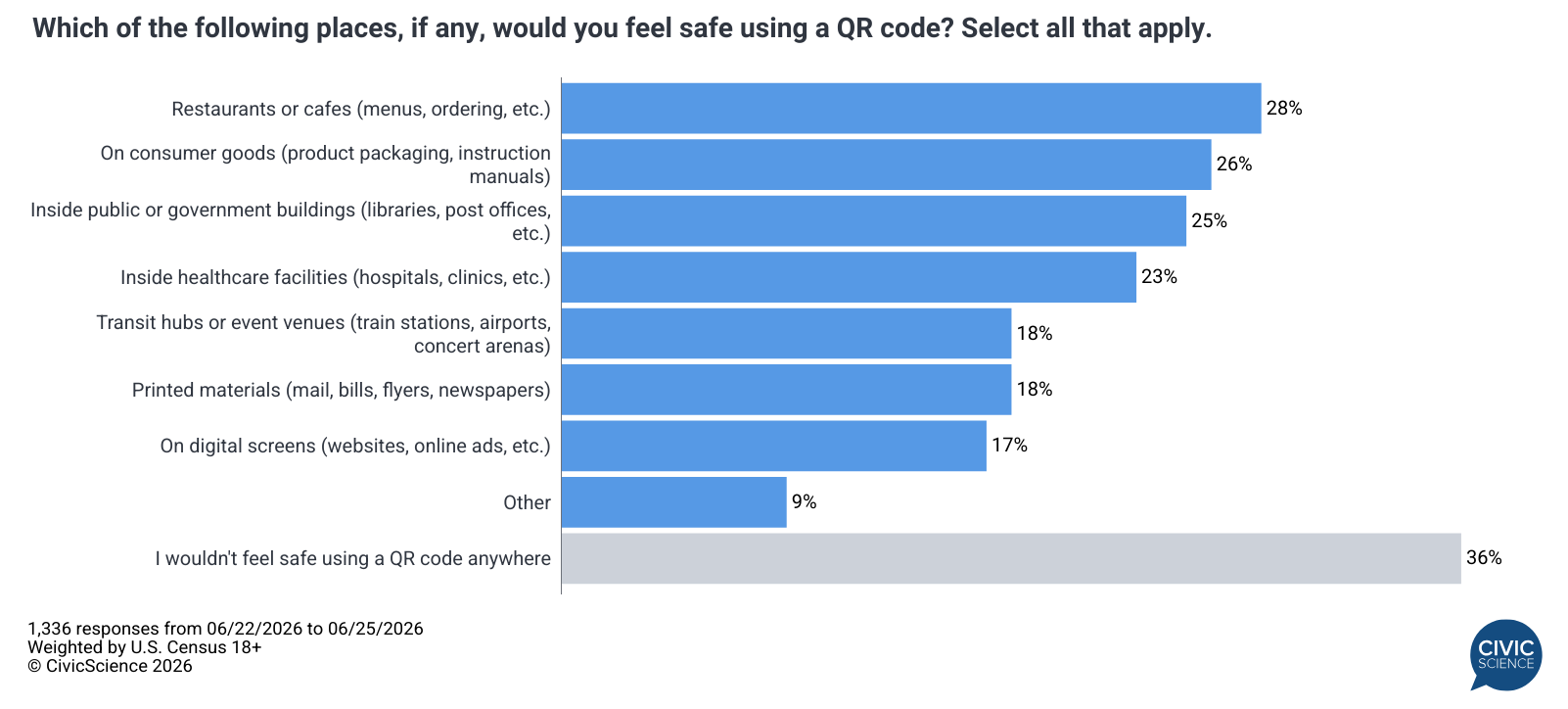

3. Consumer trust in QR codes depends heavily on context, with traditional environments like restaurants seeing the highest comfort levels among the Gen Pop.

Consumer comfort regarding QR code safety reveals a general sense of caution among the public. While just over one in four U.S. adults feel safe scanning QR codes in controlled, traditional settings like restaurants (28%) or on product packaging (26%), trust plummets when moving to public transit hubs (18%) or digital screens (17%). The most striking finding is that 36% of all U.S. adults say they would not feel safe using a QR code anywhere—a sentiment driven overwhelmingly by those 65 and older, with 65% of whom skeptical of any application. For businesses implementing QR code technology, reinforcing security and providing alternative options remain vital for older consumers’ adoption.

Weigh In: How concerned are you, if at all, about your privacy when it comes to using QR codes?