This is just a tiny glimpse of the data available to CivicScience clients. Discover more data.

The current state of economic uncertainty amid ever-evolving tariff policies continue to shape consumer behavior. As price increases loom across the retail sector, one key example is the growing demand for Buy Now, Pay Later (BNPL) services. But with growing demand comes mounting debt and the risk of falling further behind. What is the latest state of American Buy Now, Pay Later usage, and what does the road ahead look like with today’s economic climate?

BNPL Usage Grows, Including Among High-Income Earners

The latest CivicScience data show that both usage and intent in Buy Now, Pay Later have risen steadily since before the 2024 holiday season. As of May 27, 37% of those aware of BNPL use these services, up from 32% in Q3 2024. The percentage of those who are planning to use BNPL has also increased, ticking up to 12% from 9% in Q4 2024. Notably, usage and intent have also increased among high-income households ($100K+), with experience rising five percentage points since late last year.

Users and intenders are particularly leery of looming tariffs – 84% of users and 83% of intenders are at least ‘somewhat’ concerned about the impact of tariffs and trade policies on their household expenses, outpacing non-users by at least eight percentage points (75%).

Among those with some BNPL debt, 50% have less than $100 worth, including 28% who have less than $50. At the same time, as much as 27% have $500 or more in BNPL debt.

Take our Poll: Do you personally find the “buy now, pay later” model appealing or unappealing?

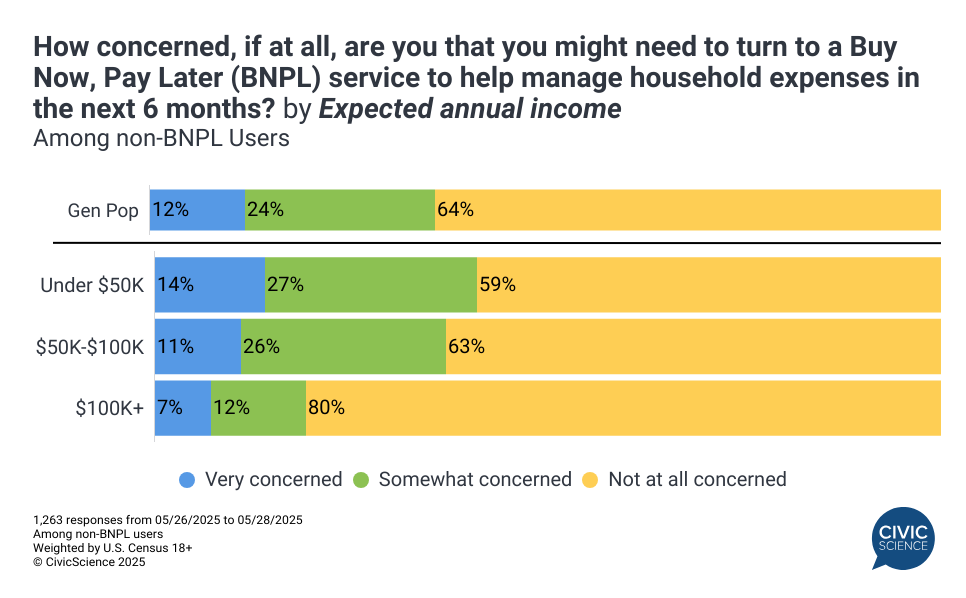

Non-Users Worry They’ll Have to Rely on BNPL to Get By

While consumers are turning to BNPL for discretionary purchases, such as live events or food delivery, additional data finds that a noteworthy percentage of Americans worry they’ll have to utilize BNPL just to get by. More than one-third (36%) of consumers who don’t currently use a BNPL service are at least ‘somewhat’ concerned they might need to turn to a Buy Now, Pay Later program to help them manage household expenses in the next six months. This concern is most common among households earning under $50K, but notably, 19% of those expecting to make $100K also share this anxiety.

Among Americans who don’t currently use BNPL, but are concerned they will need to start using them in the next six months, 77% have at least one other form of debt. Given how common credit cards are, it is unsurprising to see credit card debt emerge as the leading form of debt among these consumers. Notably, at least one in five also has a mortgage or an auto loan. Student loans, a source of stress of their own, also rank toward the higher end of common debt held by these Americans. Buy Now, Pay Later could be making for an appealing due to a lack of fees or credit checks (in some cases) and predictable payments which is why those with other forms of debt may turn be open to turning to them.

Weigh In: Do you think “buy now, pay later” services are generally positive or negative?

But Being on the Brink Isn’t Stopping All Spending

Compared to those who aren’t concerned about using BNPL to manage expenses, CivicScience data show those fearful they’ll soon need to turn to BNPL are:

- More than 3x as likely to say they’ve become ‘less’ price sensitive over the past year.

- More than twice as likely to favor ‘brand’ over ‘price’ when they are shopping.

- Nearly 30 percentage points more likely to plan on traveling in the next three months.

Despite these characteristics, these consumers are particularly vulnerable and anxious about the current economic climate of volatility. Ninety-one percent of those concerned say they’ll have to use BNPL to help them get by, and they are also concerned about the impact of tariffs on their household expenses. This concern may be fueling switching behavior—consumers who worry they’ll need to rely on BNPL to get by are significantly more likely than their unconcerned counterparts to switch banks within the next three months.

Use this Data: CivicScience clients use real-time data like this to identify high-risk, high-opportunity consumers and move quickly to engage them before they churn.

Rising Buy Now, Pay Later usage—that spans across all income levels—underscores how economic anxiety is reshaping financial behavior among Americans. Even consumers who aren’t yet using BNPL are bracing for the very real possibility, revealing just how deeply current conditions are straining household budgets and prompting shifts in spending and loyalty.