CivicScience engages directly with consumers, collecting over one million survey responses daily, to turn real-time insights into high-performing advertising campaigns. See how leading brands use CivicScience to drive campaign performance here.

When it comes to the financial landscape in 2026, navigating consumer perception is key for brands, advertisers, and media publishers who want to cut through the noise and stay top-of-mind for their audiences.

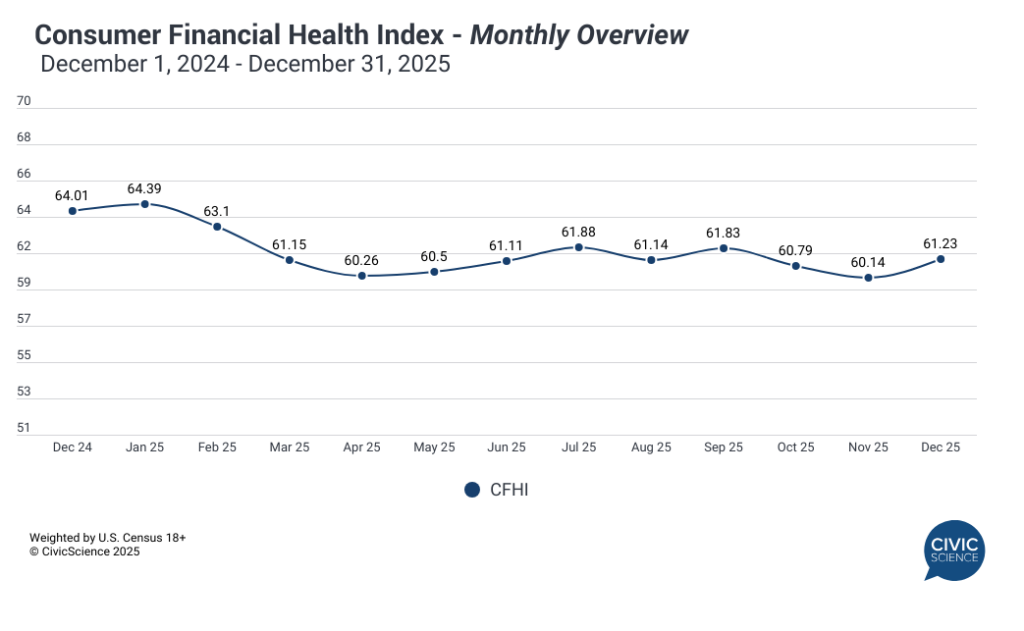

Fortunately, the CivicScience Financial Health Index (CFHI) does exactly that–by offering insight into consumers’ self-reported financial outlook in response to events on the world stage, in real-time. This crucial data equips decision-makers with the information to hone in on their messaging, anticipate spending behavior shifts, and cast a clear vision during tumultuous times. The last monthly reading of 2025 shows that consumer financial health increased 1.09 points to 61.23, marking the highest positive month-over-month shift in 2025. It’s important to note that a December increase is not unusual for the CFHI and tracks with every year in the post-pandemic era. Despite this uptick, consumer financial health still remains 2.78 points lower than it was in December 2024. This increase in optimism was reported across all age groups, but was most pronounced among adults aged 45-54, the same age group that led the decrease in November 2025.

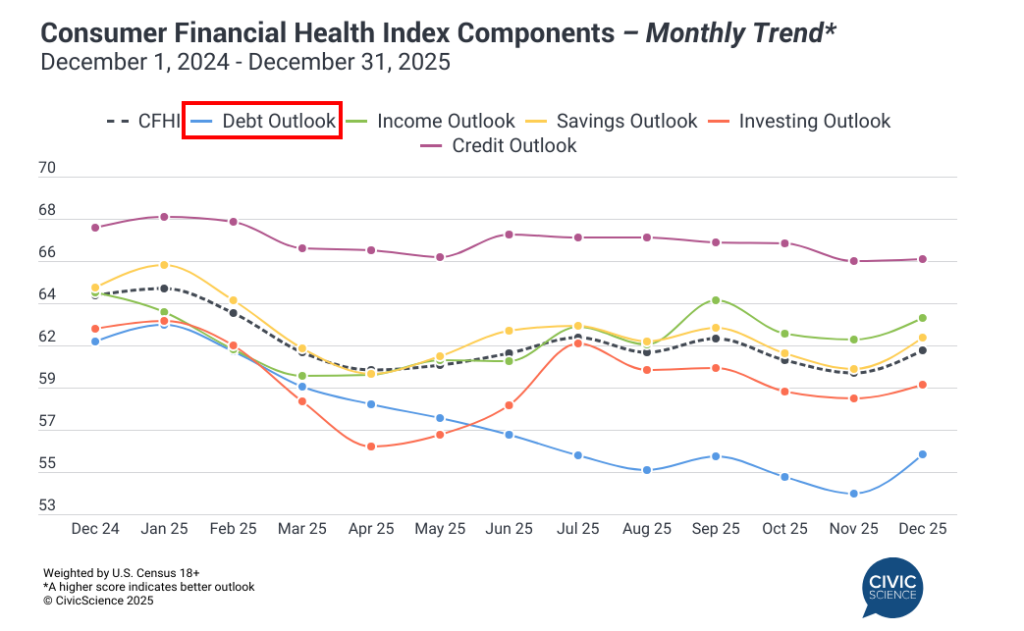

Debt Outlook Drives the Increase

The CFHI’s individual components in December reveal increases in every category, led by debt outlook (+1.93 points). Savings and income outlooks also rose by over one point (1.56 and 1.03, respectively). Meanwhile, investing outlook increased by 0.67 points, and credit outlook–which saw a rare drop in November–registered a slight 0.03 point increase.

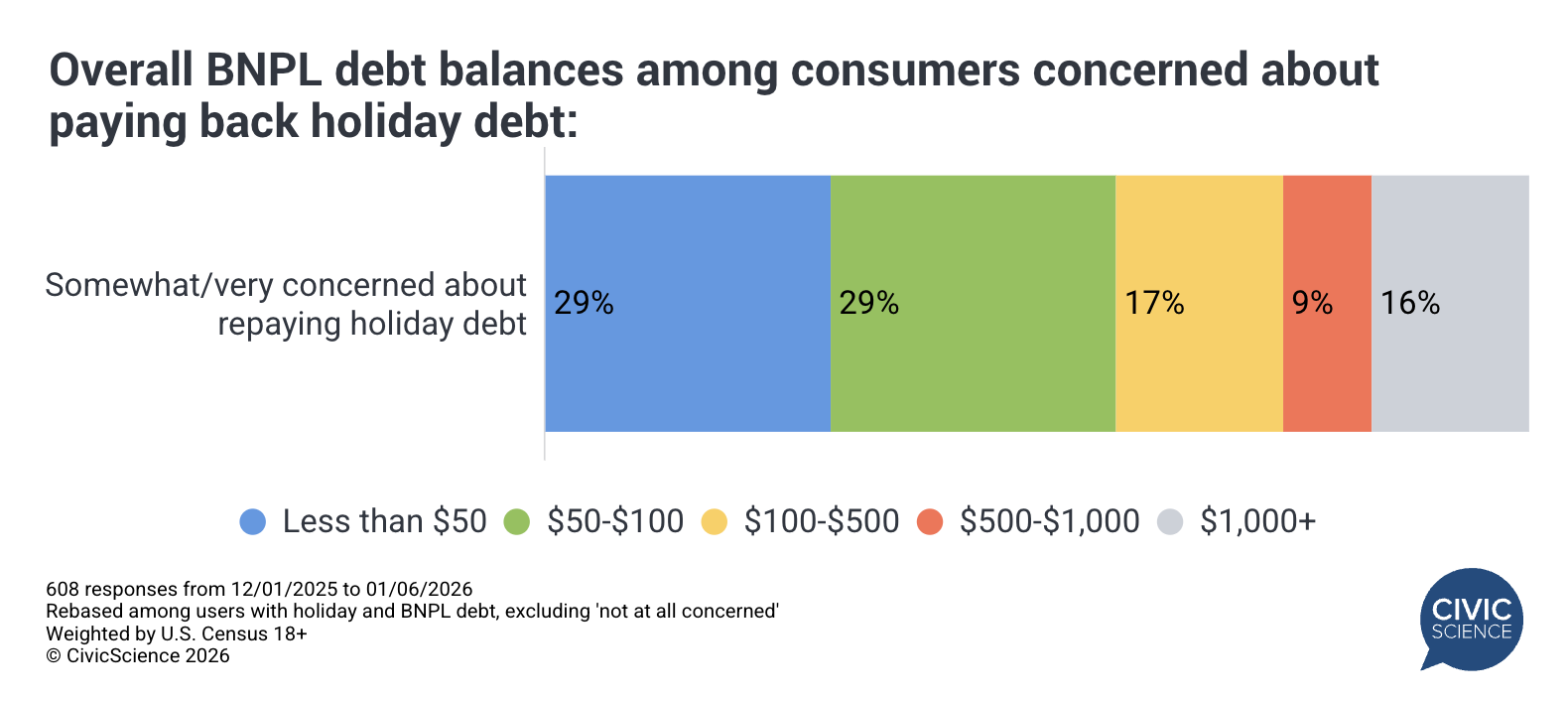

Shoppers Express Concern Over Holiday Debt Repayment

While overall consumer financial health improved in December, the data suggest that much of this optimism reflects how consumers felt in the short term, rather than how they expect to feel once post-holiday bills come due. Among respondents carrying holiday-related debt, nearly 6 in 10 (59%) say they are at least ‘somewhat’ concerned about their ability to repay it, up 10 points from concerns two years ago. Gen Z and Millennials report the highest levels of concern, highlighting early signs of financial strain beneath December’s more optimistic topline reading.

While most respondents concerned about repaying holiday debt say they owe under $100 in Buy Now, Pay Later balances this year, a substantial 24% report balances exceeding $500. Three-quarters of this group also say they’ve had to rely (or turn to) credit cards to cover gas, groceries, and other essentials in the past 365 days. Overall, this disconnect between December’s improved confidence and ongoing repayment pressure suggests optimism may be partly fueled by deferred payments — with the true weight of holiday spending likely to surface in the months ahead.

After a series of months in decline, December brought a glimmer of optimism as the CFHI saw a slight increase throughout the month amid the holiday season. However, historical trends suggest this bump may be short-lived, particularly as holiday debt bills loom and many consumers report difficulty meeting their essential needs without the use of credit cards. How this impacts consumer behavior for Q1 2026 isn’t clear yet, but those with access to these real-time insights, like CivicScience clients, will have the upper hand in staying ahead of the curve.