What’s old is new.

I just hobbled back from CES in Vegas, where New Year’s resolutions go to die. It was mostly indistinguishable from all the other times. Still exhausting and super-crowded, but also an incredibly efficient way to knock off a ton of valuable meetings in one fell swoop.

The novelty of seeing people in the flesh hasn’t worn off yet, although it felt a bit more natural. Like clockwork, I got slaughtered by a blackjack dealer at the Aria. Things went much better at Caesar’s, where Tara and I once had a run of cards for the ages.

It felt like January 2020 again, in one respect. Everybody was talking about Google killing third-party cookies.

If you aren’t in the media or advertising trade – or a cover-to-cover Wall Street Journal reader – you may have missed last week’s article about Google’s long-anticipated elimination of the pesky and nefarious bits of code that stalk us around the internet. Five years after Google first made noise about it (and at least six times I’ve written about it), the process has officially begun.

People are freaking out about it. Why? I’m not sure. It’s not like there wasn’t a fair warning. Maybe since Google delayed it a few times, there was hope they’d kick the can for eternity. Or maybe people were duped into believing an equivalent surveillance mechanism would fill the void.

All I know is the advertising world is fixing to get rocked. And, if you’re an internet user, a trusted media outlet with quality content, or an advertiser, publisher, or tech company who prepared for it, prosperous days are ahead. Prayers for the rest of you.

Advertising isn’t the only industry hurtling back to the future. Did you know 1-in-10 Americans – and quickly rising – now get their live TV by way of a digital antenna? For a one-time cost under $100, you can get 160+ channels fed to every device you own. Sure, you still need to pay for Netflix, Apple TV, et cetera. But traditional TV is trending toward free – over the air.

With all the mind-blowing gadgets scattered across the Las Vegas Convention Center this year – check out Samsung’s translucent TV – we’re reminded that not all innovation is progress. Some truths can’t be outsmarted: People value their privacy. Lower costs always win, eventually. Connecting in person is better than Zoom.

And never, ever hit a hard 17.

Here’s what we’re seeing:

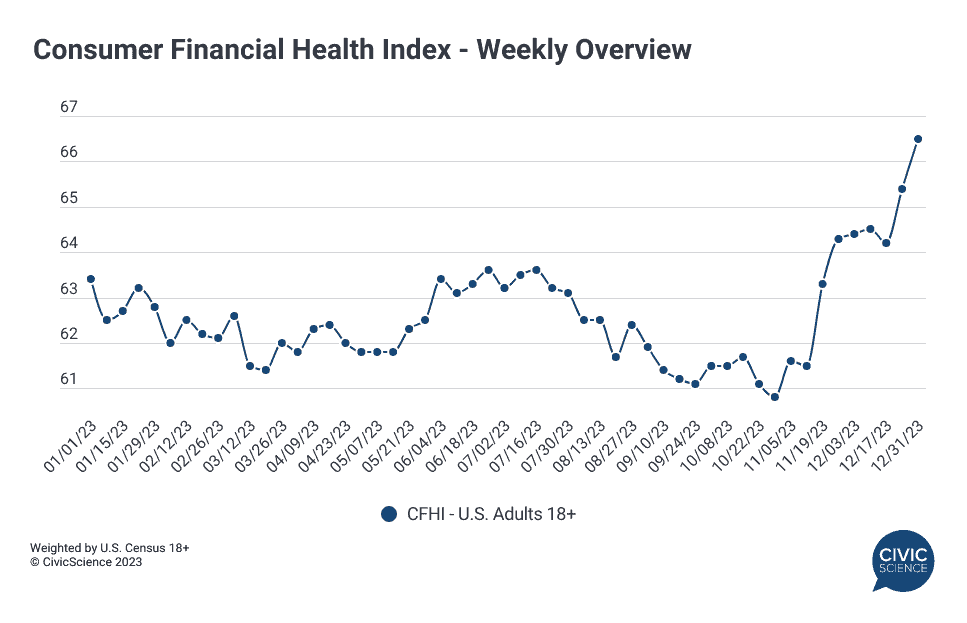

The personal financial outlook of Americans ended 2024 on a high note. Our Consumer Financial Health Index continued its late-year surge through December, with U.S. adults reporting rosy sentiments about their current and future money matters. People had markedly improved optimism for their income, credit, investments, and savings – while debt outlook remains shaky (and will likely worsen in coming months). Things aren’t quite back to where they were at the end of 2021, but it’s getting close.

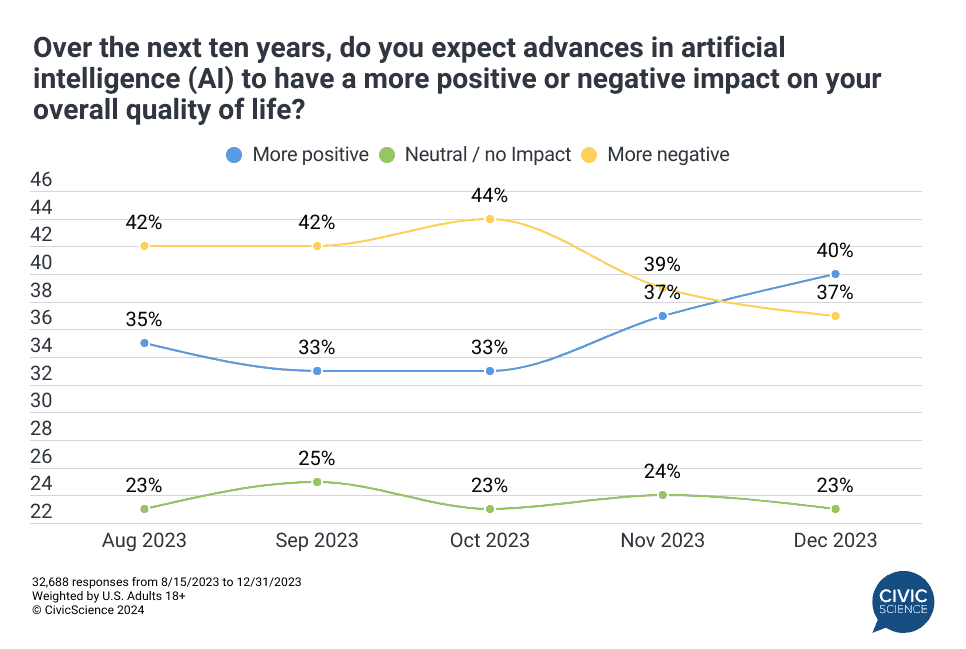

People are also feeling more optimistic about AI. In our 3 Things to Know this week, we highlighted our latest tracking data on Americans’ attitudes about artificial intelligence. While 8-in-10 adults remain at least somewhat concerned about the safety and economic (job loss) implications of AI, hopes that will have a net positive effect on our quality of life are on the rise. We also looked at the explosion of subscription services people employ and the popularity of homemade and “upcycled” gifts this past Christmas.

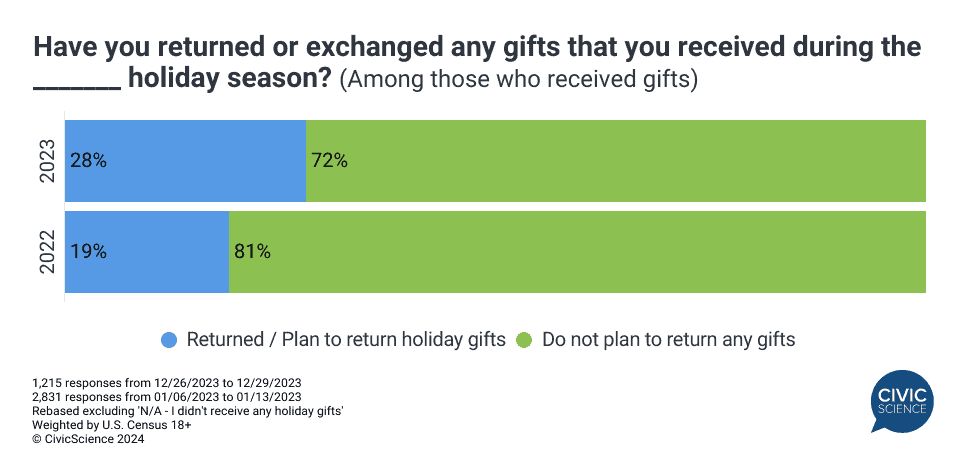

In related news, I guess people sucked at buying Christmas presents this year. Twenty-eight percent of Americans say they’ve already returned at least one of their holiday presents this year (or plan to), representing a 47% jump from this time last year. The biggest ingrates were men, people making over $100k, and Gen Zs – 59% of whom fall into the “returner” segment. Try harder next year, folks.

The holidays stopped some Ozempic-borne trends in their tracks. The commercial success of our new GLP-1 consumer tracker is only surpassed by the diversity of the companies who’ve signed up for it – coming from an array of industries I wouldn’t have guessed. One area where the potential impact of Ozempic and its peers might be overblown, at least recently, is the snacking category. GLP-1 users reported higher rates of munching all manner of snacks, sweet and savory alike, between October and December. Christmas gorging remains undefeated.

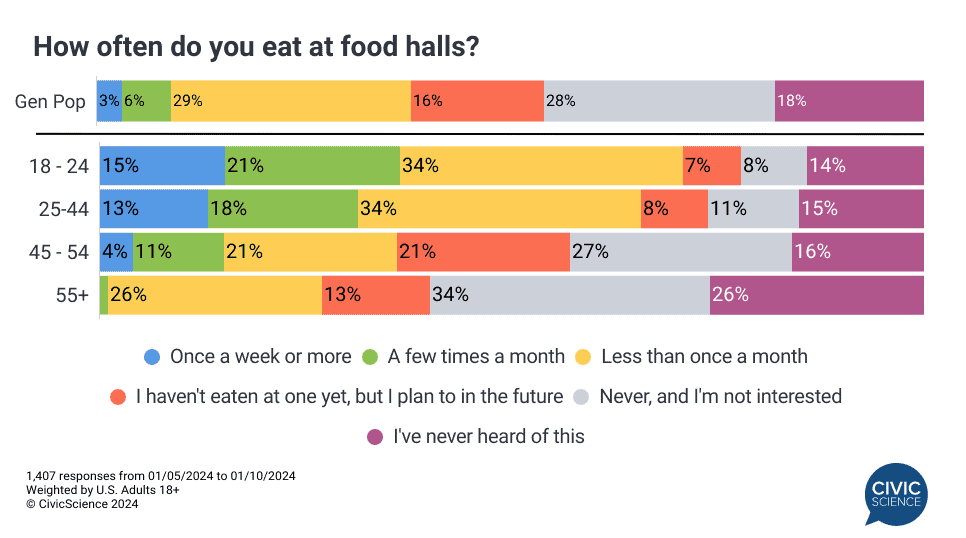

Food halls are all the rage. With mall food courts going the way of the landline telephone, a surge of trendier dine-in venues showcasing local and independent restaurants is happening all over America. With an estimated 340 food halls open across the country, another 127 are expected to open in 2024. Driving the craze – of course – are Gen Zs and Millennials, particularly urban dwellers and hybrid workers. The generally higher cost of these venues doesn’t seem to be keeping people away.

More awesomeness from the InsightStore™:

- How to tell the difference between Estée Lauder and L’Oréal customers;

- Ikea shoppers and Bed Bath & Beyond shoppers are very different;

- Peloton subscribers are 4X more likely to shop at Sephora, research where companies stand on social issues, and other key insights.

The most popular questions this week:

How often do you feel like there’s nothing to watch?

Would you say you have more or fewer life regrets than others?

Do the books in your home serve more of a functional or decorative purpose?

Has social media changed the way we live our lives for better or worse?

Answer Key: Not often lately; I’d like to think fewer; Decorative; For sure; Way worse.

Hoping you’re well.

JD

Want to see weekly insights from the What We’re Seeing through the lens of your customers? Learn how here.

Was this email forwarded to you? Sign up here. If you are new to this list, check out our Top Ten to get caught up.