News outlets do have a fighting chance.

Just not all of them.

Notwithstanding the extreme flank of our political spectrum who are deeply suspicious of all formal education and expertise, the rest of America knows that professional journalism is essential to our society. The question is how to preserve it.

One challenge is that many people have lost the ability to discern quality journalism from the alternative. Real or perceived biases of major outlets have steered audiences toward lower-tier publishers that cater to their beliefs. I’m an expert if you agree with me, a nut-job or political shill if you don’t.

Another challenge is the competition news publishers face for advertising dollars today. Google, Meta, and YouTube suck so much oxygen out of the room, everyone else is gasping. Pandering to the biases of a narrow audience becomes life support. Relying on kickbacks from tools like Taboola and Outbrain – who often drive traffic to the lower-tier publishers mentioned above – amounts to intubation. Maybe those are melodramatic metaphors. Maybe not.

Any publisher who can thrive on the proceeds of a paying subscriber base should keep doing what they’re doing. The New York Times, The Atlantic, The Wall Street Journal, and the Financial Times (and others) fit this bill. Notably, their audiences skew highly educated and/or affluent, meaning they can discern and appreciate quality journalism – and afford to pay for it.

Alas, that solution alone exacerbates the knowledge gap between haves and have-nots. It’s not enough.

The best chance for the remainder of the news media is scale – which likely comes from consolidation. Nexstar’s pending acquisition of Tegna is a good example. Opponents of the merger fear it will stifle competition, citing the National Television Ownership Rule that prohibits a single entity from owning TV stations reaching more than 39% of US households. It’s archaic. Local news outlets aren’t really competing with each other, at least not nearly to the extent they’re competing with Google and Meta – who have no arbitrary cap on the households they can reach.

The benefits of greater scale are Econ 101. Reducing overhead is the unfortunate, but necessary and much smaller advantage. Some jobs will be lost – but that’s happening anyway.

The bigger gains come from expanded and streamlined sales power. News outlets – particularly local ones – don’t lag the big tech platforms in the performance of their ads. We see this first-hand in the advertising we run across our publisher partner footprint. What small publishers lack individually is reach and ease of execution – advertisers and agencies would rather do one direct deal than 100. Moreover, with a stronger balance sheet, larger news companies can invest in technology, innovation, and measurement like few can today.

The second-order effects are admittedly double-edged. Winnowing competition too far is bad. A city like Pittsburgh – having lost population for 8 straight decades – struggles to support five major news outlets (3 TV stations and 2 newspapers). But we need more than one. Allowing for a multitude of voices in the press while ensuring the sustainability of any is a difficult mission. I also don’t know how the losers and winners should be decided. But it must happen.

Otherwise, everyone will lose.

Here’s what we’re seeing:

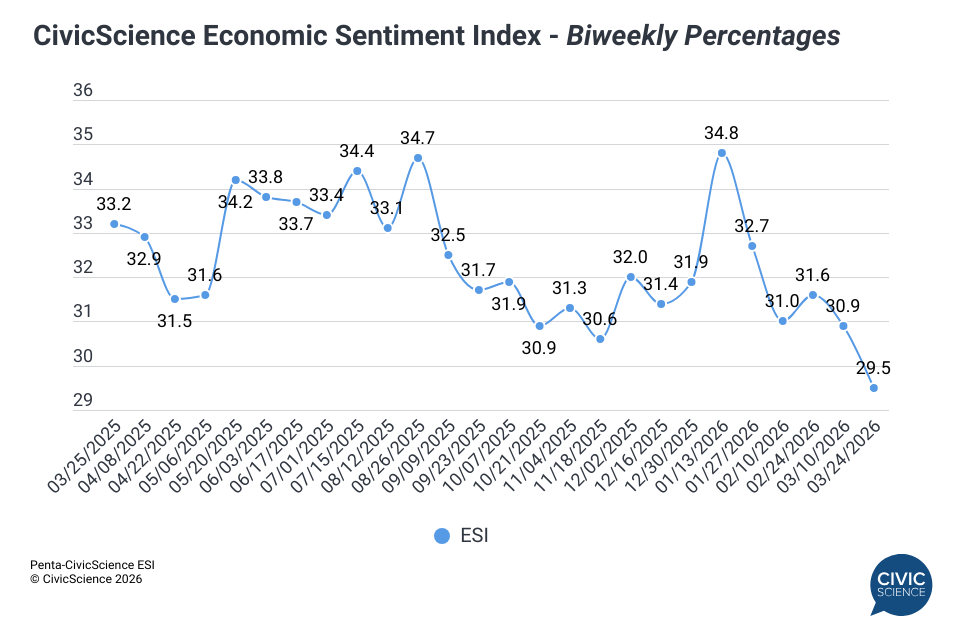

While I was away last week, consumer confidence hit the lowest point we’ve ever seen. I must admit, I was a little surprised to see the Conference Board report this week, showing that their March number increased – ours makes way more sense. Our Economic Sentiment Index over the final two weeks of March hit unprecedented (since 2013) depths, on the backs of major drops in confidence around major purchases and homes, as well as continued glumness over the job market. For what it’s worth, long-term hopes for improvement in the U.S. economy were slightly above water – perhaps suggesting a hint of “nowhere to go but up.”

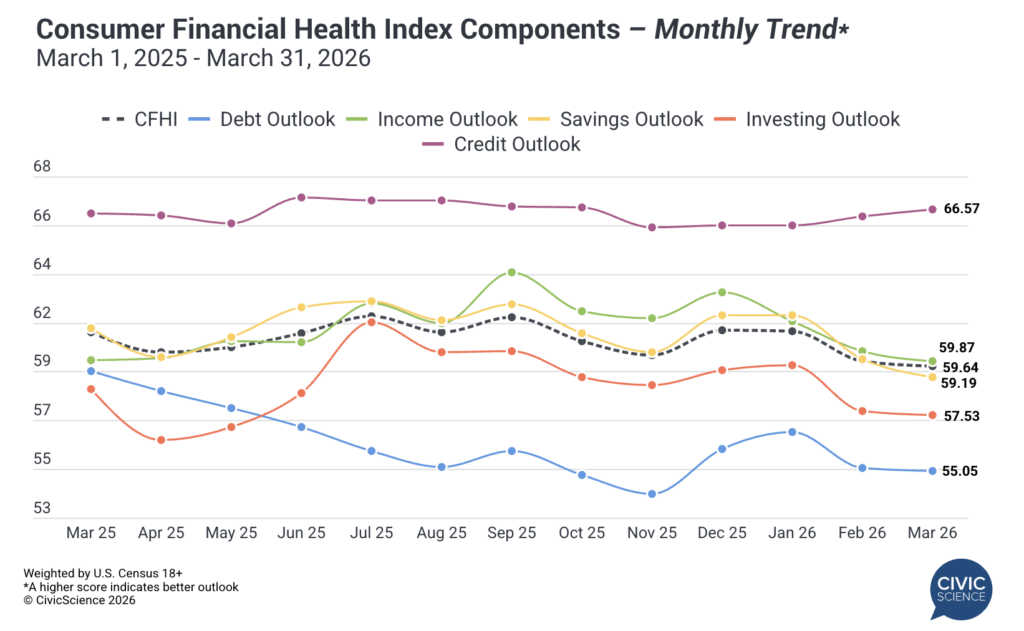

Meanwhile, consumer financial health in March was much less troubling. This may explain the Conference Board disparity, since their metrics lean a bit more heavily toward the personal financial state of consumers (as opposed to the macro outlook). Our Consumer Financial Health Index for the full month of March fell only slightly, as Americans’ debt and income concerns stabilized, while personal credit outlook improved – perhaps because everyone paid off those holiday credit card bills. It also aligns with the modest but better-than-expected report on February retail sales (which I’ll bet you $1 are eventually revised downward). Anyway, people are feeling okay about their economic state, but pessimistic going forward.

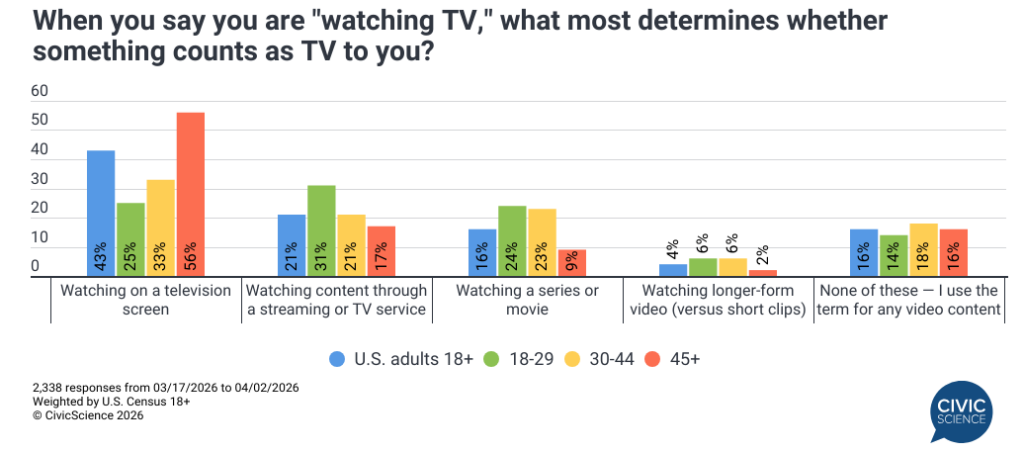

People are watching more TV than they ever have before – depending on how you define TV. In a new study spawned by my brilliant business partner Gretchen, we found that America’s TV habits (and vernacular) are fragmenting in fascinating ways. While the number of Americans who watch television 4+ hours EVERY DAY has grown by 35% since 2023, the percentage who watch zero TV (11%) is growing as well. More interesting, however, is how the notion of “watching TV” is changing dramatically by generation. For the majority of people 45 and older, it means “literally” looking at a TV screen. For the majority of people under 45, meanwhile, it means everything from streaming TV shows to watching movies to longer-form videos online.

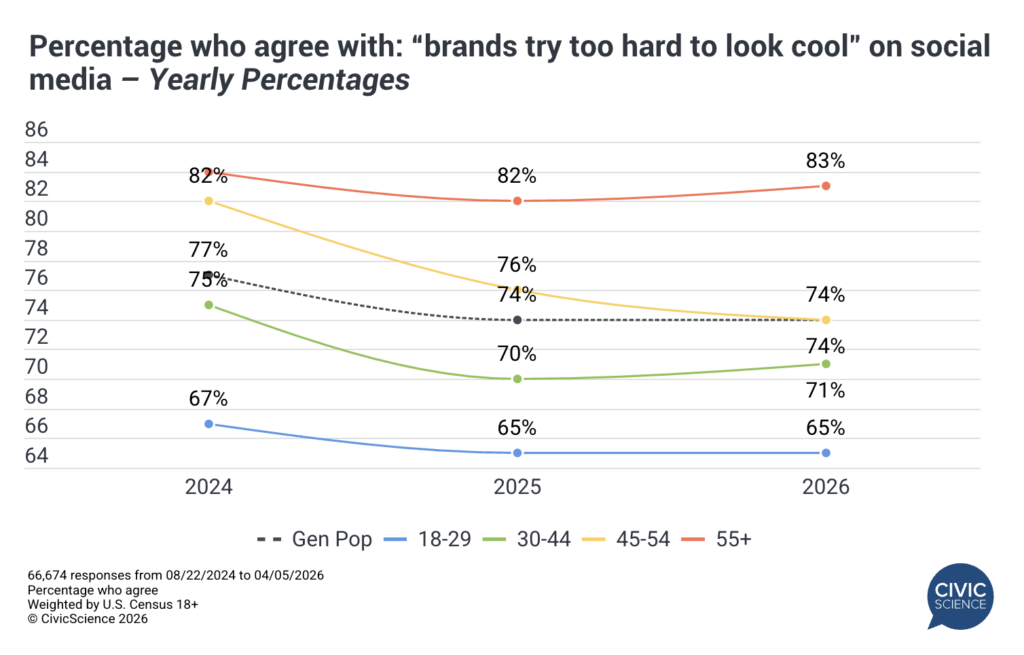

Most brands trying to look cool on social media are achieving the opposite. We published a study this week looking at the effectiveness of advertising “coded” for Gen Z and Gen Alpha. In short, it can work – so long as nobody outside of those generations sees it. The use of Gen Z and Gen A slang in marketing, for instance, has a net positive (barely) impact on those cohorts. Everyone else finds it very cringe. But even those younger age groups think brands try way too hard to be cool, meaning the authenticity is missing. Tread lightly, my friends.

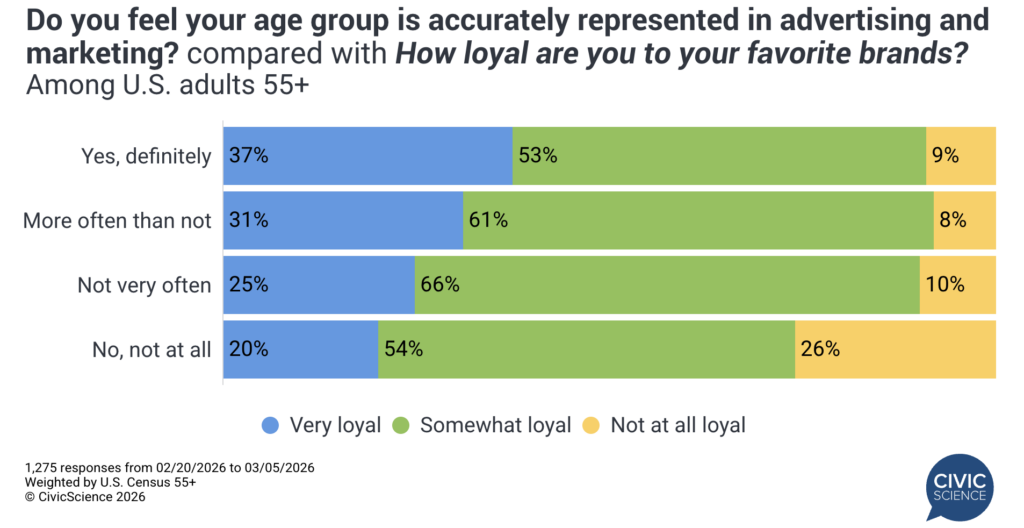

And in related news, older Gen Xers and Boomers (the groups with all the money right now) are feeling woefully underrepresented in marketing. Brand loyalty among older Americans has fallen to a 7-year low, a noteworthy finding because, historically, we expect that cohort to lock in with their favorites after playing the field their whole lives. One big factor that seems to be driving the trend is their feeling of being forgotten by marketers. The number of Xers and Boomers who don’t feel accurately represented in marketing has jumped 58% since 2023. The ones who do are more loyal to their favorite brands. It’s as simple as that.

More awesomeness from the InsightStore™:

- 3 Things to Know from this week: How rising gas prices are impacting tax refund plans, how recent major weather events are impacting eco-anxiety, and how seemingly everything is causing air travel reticence;

- 3 Things to Know from last week: People are increasingly narrowing their friends and romantic prospects based on politics, social media influencers drive a lot of consumer travel and services, and prediction markets still have tons of untapped upside, except among Gen X.

- The economic climate weighed on Easter holiday plans;

- Excitement in the newly launched MLB season is up healthily over last year;

- A lot of people shopped Amazon’s Big Spring Sale event to find deals on beauty and health purchases.

The most popular questions this week:

Do you prefer to dine at restaurants that have a formal dress code or a more casual vibe?

Do you prioritize gut health in your overall wellness routine?

Have you ever thought about owning a bar or tavern?

How would you grade yourself in terms of being a good partner?

Answer Key: Colleges should do it; I like to mix it up; No but after 5 days eating in Mexico, I think I might; It’s like a boat – better when your friends own them; Hopefully Tara would bet the over on 8.

Hoping you’re well,

JD